Global financial markets closed out May 2026 amid one of the most dynamic and eventful trading environments of the year. Three dominant themes shaped investor sentiment throughout the week: geopolitical developments in the Middle East, evolving expectations for U.S. monetary policy, and the continued artificial intelligence-driven surge in technology stocks.

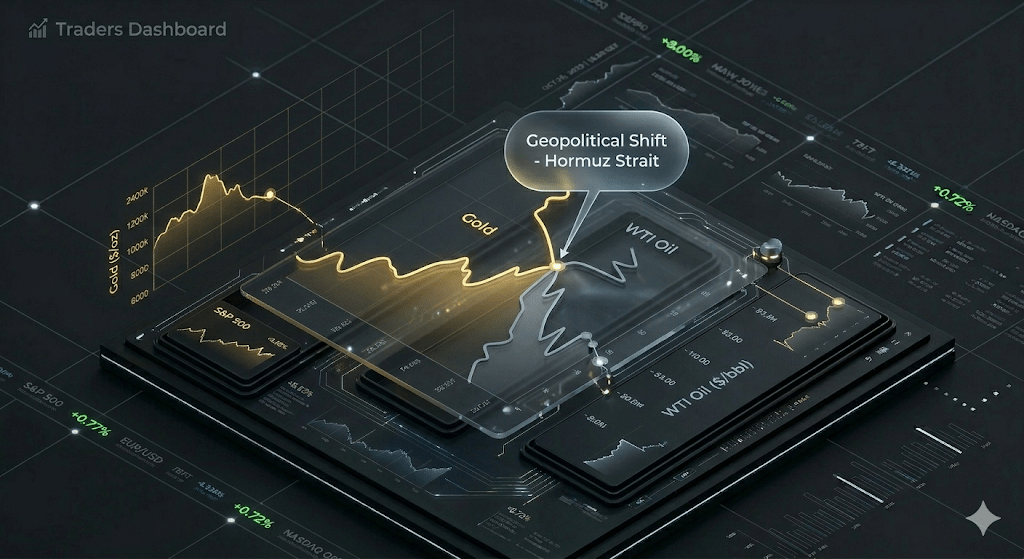

Negotiations involving the United States and Iran regarding maritime security and the future of shipping flows through the Strait of Hormuz became the primary driver of commodity and currency markets. Every new headline, diplomatic leak, or indication of progress toward de-escalation triggered significant swings across oil, gold, and foreign exchange markets.

At the same time, U.S. inflation data offered investors a mixed picture. Price pressures remained above the Federal Reserve’s long-term target, but the figures were not strong enough to eliminate hopes that monetary conditions may eventually ease. As a result, markets remained caught between confidence in continued economic growth and concerns that inflation could reaccelerate during the second half of the year.

Despite this backdrop, U.S. equities delivered another remarkable performance. Major indexes ended May at or near record highs, supported by strong corporate earnings, resilient consumer spending, and continued enthusiasm surrounding artificial intelligence investments.

1. U.S. Equities: Wall Street Enters a New Phase of Optimism

American equity markets finished the final week of May with fresh record highs, extending one of the strongest rallies seen in recent years.

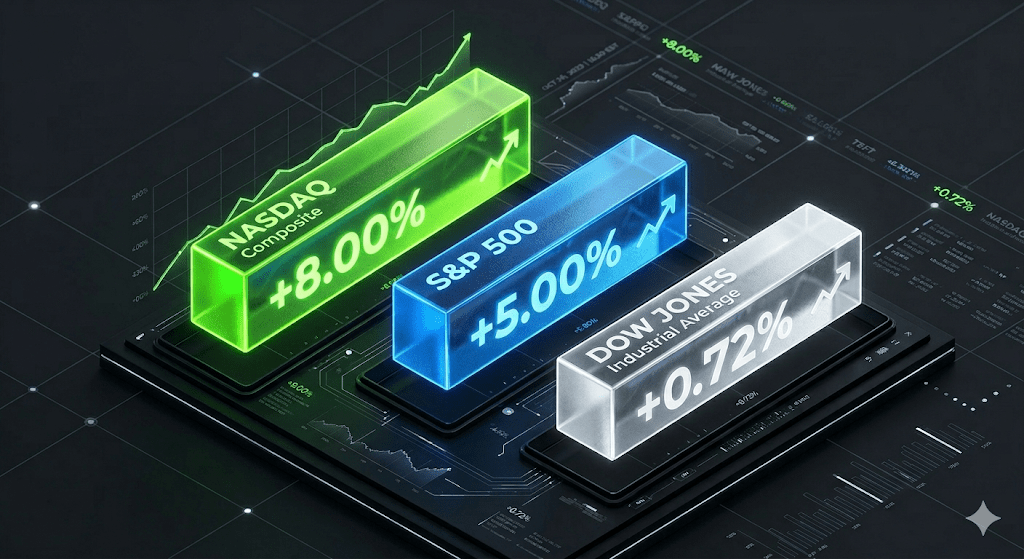

The Dow Jones Industrial Average closed above the 51,000-point mark for the first time in history, while the S&P 500 recorded its ninth consecutive week of gains. The Nasdaq Composite also delivered one of its strongest monthly performances of 2026, benefiting from sustained momentum in technology and AI-related stocks.

Market estimates indicate that the S&P 500 gained more than 5% during May, while the Nasdaq advanced close to 8% for the month. Investors continued to reward companies demonstrating strong earnings growth, pricing power, and direct exposure to the expanding artificial intelligence ecosystem.

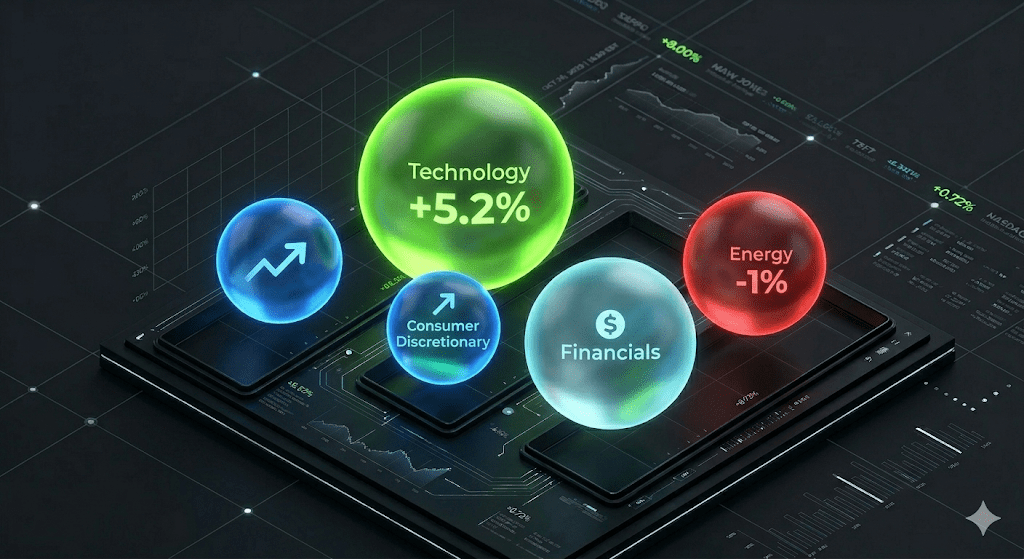

Importantly, the rally broadened beyond the so-called “AI winners.” Industrial firms, financial institutions, travel-related businesses, and selected small-cap companies also participated in the advance. Many strategists viewed this broadening market participation as a healthier sign than rallies driven exclusively by a handful of mega-cap technology stocks.

Artificial Intelligence Remains the Market’s Central Theme

Artificial intelligence continued to dominate corporate earnings discussions and investor allocation decisions.

Dell Technologies emerged as one of the standout performers after reporting exceptionally strong demand for AI-optimized servers and data-center infrastructure. Spending on computing power, cloud capacity, and AI deployment remained a major source of revenue growth across the technology sector.

Meanwhile, partnerships between cloud-service providers and AI developers fueled expectations that the current investment cycle may extend well beyond 2026. Investors increasingly view AI as a multi-year structural trend rather than a short-lived market phenomenon.

However, not every technology company benefited equally. Some software firms faced pressure as investors questioned whether AI agents and automated digital assistants could disrupt existing business models and reduce demand for traditional enterprise software solutions.

Valuation Concerns Begin to Surface

Despite the strength of the rally, valuation concerns are becoming more visible among institutional investors.

Several major investment houses have warned that equity markets appear increasingly priced for perfection. Current valuations assume:

A gradual decline in inflation.

Continued economic expansion.

No major geopolitical shocks.

Sustained AI-driven corporate spending.

Stable financial conditions.

Any significant disappointment in one or more of these assumptions could trigger increased volatility during the summer months.

2. U.S. Treasury Market: Renewed Focus on Bonds

The Treasury market experienced an active week as yields retreated from recent highs.

The yield on the benchmark 10-year U.S. Treasury note declined toward 4.46% by Friday after approaching 4.70% earlier in May, its highest level in more than a year. The move reflected improving risk sentiment and reduced concerns over global energy disruptions.

The Yield Curve Moves Toward Normalization

One of the most closely watched developments was the continued normalization of the Treasury yield curve.

The spread between long-term and short-term Treasury yields turned positive after an extended period of inversion. Historically, an inverted yield curve has been considered one of the most reliable indicators of a future recession.

Although normalization does not eliminate recession risks, it suggests that investors are increasingly adjusting to the prospect of higher interest rates without an immediate economic collapse.

Growing Debate Over the Role of Bonds

Large asset managers continue to debate whether government bonds can still serve as an effective hedge against equity-market declines.

For decades, investors relied on the traditional 60/40 portfolio model, combining stocks and bonds to reduce volatility. However, recent years have demonstrated that periods of elevated inflation can hurt both asset classes simultaneously.

As a result, portfolio managers are increasingly reassessing diversification strategies and seeking alternative sources of risk protection.

3. Crude Oil: The War Premium Continues to Fade

Oil remained among the most volatile asset classes throughout the week.

West Texas Intermediate crude fell below $88 per barrel, while Brent crude also moved lower as traders increasingly priced in the possibility of diplomatic progress involving Iran and shipping routes through the Strait of Hormuz.

Markets interpreted potential improvements in regional stability as likely to:

Reduce geopolitical risk premiums.

Improve global shipping flows.

Lower the probability of supply disruptions.

Ease concerns regarding energy security.

Nevertheless, the decline was not entirely linear.

Toward the end of the week, oil prices rebounded temporarily following reports of renewed military tensions in Lebanon and concerns that broader regional instability could once again threaten energy markets.

Outlook

From an analytical perspective, crude oil remains at a critical juncture.

A sustained diplomatic breakthrough could push prices lower during June, particularly if global demand expectations soften.

Conversely, any deterioration in negotiations or escalation of regional conflict could rapidly restore the geopolitical premium that has supported oil prices throughout much of 2026.

4. Precious Metals and Copper: Inflation Versus Interest Rates

Gold ended the week modestly higher, maintaining its appeal as a defensive asset despite the strength of U.S. equities.

The precious metal benefited from:

Ongoing geopolitical uncertainty.

Periodic weakness in the U.S. dollar.

Continued demand for safe-haven assets.

However, expectations that the Federal Reserve may keep interest rates elevated limited gold’s upside potential.

Higher real yields increase the opportunity cost of holding non-yielding assets such as gold, creating a persistent headwind for the metal.

Silver remained significantly more volatile than gold due to its dual role as both an investment asset and an industrial metal. Price swings reflected changing expectations regarding economic growth, manufacturing demand, and geopolitical developments.

Copper prices, meanwhile, remained under pressure as investors balanced optimism surrounding infrastructure spending, renewable energy projects, and AI-related data-center construction against concerns about slowing global growth.

5. Global Currencies: The Dollar Loses Some Momentum

The U.S. Dollar Index ended the week slightly lower after a period of heightened volatility.

Two primary factors contributed to the move:

First, improving market sentiment reduced demand for defensive dollar positions.

Second, investors increased bets that the Federal Reserve may be approaching the final stages of its current tightening cycle.

The euro strengthened against the dollar as investors rotated into European assets and reduced safe-haven exposure.

Meanwhile, the Japanese yen remained under pressure due to the substantial interest-rate differential between the United States and Japan. Higher U.S. yields continue to encourage capital outflows from Japan and support carry-trade strategies.

Many currency strategists believe the yen will remain highly sensitive to any unexpected policy adjustments from the Bank of Japan in the months ahead.

6. Digital Assets: A Period of Reassessment

The cryptocurrency market entered a more challenging phase during May.

Following a powerful rally earlier in the year, investors increasingly engaged in profit-taking and portfolio rebalancing activities.

Bitcoin finished the week near $73,600, remaining well below the highs recorded earlier in the month.

One of the most important developments was the continuation of outflows from spot Bitcoin exchange-traded funds in the United States. These outflows raised questions about the sustainability of institutional demand that had helped drive prices higher during previous quarters.

Is Institutional Demand Slowing?

The ETF outflows sparked debate regarding the long-term strength of institutional participation in digital assets.

Some analysts believe the withdrawals primarily reflect short-term positioning changes driven by interest-rate expectations rather than a fundamental shift in sentiment toward Bitcoin.

Others argue that the market may require a new catalyst before attempting another major move higher.

For now, investors continue to monitor fund flows, regulatory developments, and broader macroeconomic conditions for clues regarding the next phase of the cryptocurrency cycle.

7. Monetary Policy and Economic Data

Inflation data remained the central focus of global investors.

The latest U.S. Personal Consumption Expenditures (PCE) report showed annual inflation running at approximately 3.8%, while core inflation remained above the Federal Reserve’s long-term objective.

Although inflation has moderated from previous peaks, policymakers continue to face challenges in bringing price growth fully under control.

Consumer spending data also indicated that American households remain relatively resilient despite higher borrowing costs and tighter financial conditions.

The Federal Reserve’s Dilemma

The Federal Reserve faces a difficult balancing act:

Inflation remains above target.

Economic growth is slowing.

Labor-market conditions remain relatively healthy.

Geopolitical developments could reignite inflationary pressures.

As a result, policymakers must carefully weigh the risks of maintaining restrictive monetary policy against the risks of easing prematurely.

Financial markets remain divided regarding the likelihood of future rate increases versus a prolonged pause.

8. Looking Ahead: Key Catalysts for June

Investors enter June facing a packed calendar of potentially market-moving events.

1. U.S. Employment Report

The May employment report will provide one of the clearest indicators of underlying economic strength.

A stronger-than-expected reading could reinforce expectations for higher interest rates and support Treasury yields.

A weaker report could revive speculation about future policy easing.

2. Federal Reserve Meeting

The June 16–17 Federal Reserve meeting is widely viewed as one of the most important policy events of the summer.

Investors will focus not only on the interest-rate decision itself but also on policymakers’ updated projections regarding inflation, growth, and future policy direction.

3. Iran and the Strait of Hormuz

Developments surrounding Iran and regional shipping security are expected to remain among the most influential geopolitical drivers of oil, gold, and currency markets.

Any significant breakthrough or setback could trigger immediate reactions across multiple asset classes.

4. Major IPO Activity and Artificial Intelligence

Investors are also closely monitoring the pipeline of major technology and aerospace offerings, including the widely anticipated SpaceX IPO.

If completed according to current expectations, the transaction could become one of the largest public offerings in modern market history and further reinforce investor enthusiasm toward innovation-driven sectors.

Global markets concluded May 2026 at a delicate crossroads. On one hand, strong corporate earnings, resilient consumer demand, and continued investment in artificial intelligence continue to support equity valuations and investor confidence.

On the other hand, elevated inflation, geopolitical uncertainty, and the possibility of additional monetary tightening remain significant risks.

Wall Street has successfully reached new record highs, but June is likely to be a more demanding test. Markets are moving beyond optimism driven by headlines and entering a phase where economic fundamentals, corporate execution, and geopolitical realities will ultimately determine whether the rally can continue.