In an extraordinary financial landscape, the week of June 22–26, 2026, combined escalating pressure, a radical shift in monetary policy, and a geopolitical truce that faltered on its eighth day. It was not merely a standard trading week, but a multi-dimensional “stress test” for the global financial system, sketching the outlines of a second half of the year that promises more volatility than stability.

I. U.S. Equities — Five Days of Pressure and a Leadership Shift

The week opened to the sound of a sustained sell-off. On Monday, the S&P 500 fell 0.37% to 7,472 points, while the Nasdaq dropped 1.32% to 26,166 points. The Dow Jones stood apart, gaining 148 points, supported by a nearly 4% rise in Caterpillar shares. Tech giants were the fuel for the decline; Alphabet shares collapsed by 5% amid concerns over talent attrition in artificial intelligence, while Amazon and Meta lost 4.8% and 2.3% respectively, and Microsoft fell 3%.

Source: Bloomberg

On Tuesday, the decline intensified as the sell-off spread globally; the S&P 500 lost 1.44% to close at 7,365 points, and the Nasdaq plummeted 2.21% to 25,587 points. Simultaneously, European markets fell sharply, with the Stoxx 600 index closing down 0.57%, and tech and mining stocks falling 3.4% and 3.3% respectively.

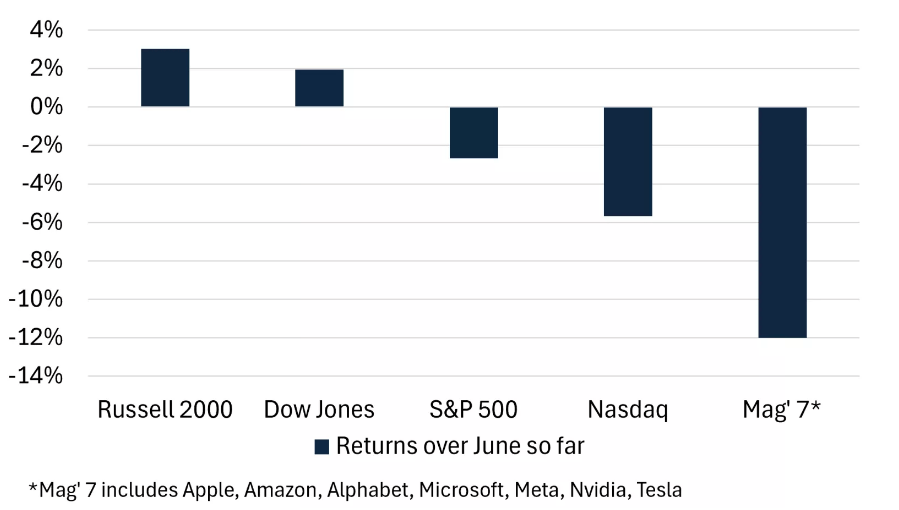

On Wednesday, the S&P 500 closed at 7,358 points and the Nasdaq at 25,476 points, in a session dominated by anticipation of Micron’s results after the close. By Friday’s end, the S&P 500 closed at 7,354 points, losing nearly 2% weekly, and the Nasdaq suffered losses of 4.6% in five consecutive losing sessions, while the Dow Jones finished the week with a 0.6% gain, the sole exception among major indices.

Sector-wise, healthcare was the top performer thanks to gains in Bio-Techne and Incyte, which exceeded 22% and 15% respectively, in what appeared to be a genuine shift in market leadership toward defensive sectors with solid fundamentals. According to John Flood at Goldman Sachs, the market remains in a “buy-the-dip” mode, confirming that retail investors were the most consistent buyers throughout 2026.

One of the greatest pressures was the SpaceX file; a New York Times report on the potential for OpenAI to delay its IPO until next year raised serious concerns about the sustainability of AI infrastructure spending amid a capital market funding crunch.

II. Micron — The Shining Exception in the Tech Storm

Amid the tech sell-off, the week’s most prominent event occurred far from the retreating markets. On June 24, Micron Technology announced its fiscal Q3 2026 results, beating expectations by a historic margin; revenue reached $41.46 billion compared to expectations of $35.69 billion, while earnings per share (EPS) exceeded $25.11 against expectations of $20.49. The stock jumped 14.55% in after-hours trading to $1,199.

Revenue rose 346% year-on-year from just $9.3 billion a year ago. More significant than the results was Micron’s signing of 16 strategic agreements with customers that guarantee a minimum revenue of $100 billion, with cash prepayments of $22 billion, signaling a structural shift that moves the company away from the traditional cyclical volatility model of the memory industry.

Future guidance was provided without a clear ceiling; management projected record Q4 revenue of $50 billion with a gross margin nearing 86%, and estimated profitability of $31 per share. Management announced that HBM3E and HBM4 memory are fully booked through 2027, with demand extending into 2028, while global supply remains unable to keep up. By Friday’s end, Micron traded between $1,119 and $1,198, with the stock achieving gains of approximately 725% over the past 12 months.

III. Oil — Risk Premium Collapse Below $70

At the start of the week on Monday, Brent crude was trading at $79.25 per barrel, down $3.2 from the previous day. The primary driver was the collapse of the geopolitical risk premium that had supported prices since February.

On Wednesday, Brent lost 4.33% to $73.74, the lowest level since before the U.S.-Israeli strikes on Iran at the end of February, while WTI plummeted 3.92% to $70.34. By the end of the week, WTI dropped another nearly 4% to settle near $69 per barrel, while Brent fell more than 4% to near $72.

However, Thursday brought a shock. The Iranian Revolutionary Guard launched an attack with four suicide drones targeting commercial ships in the Strait of Hormuz, hitting a Singaporean cargo ship in its upper section with reported structural damage but no human casualties. After Trump stated hours later that it was a “foolish violation,” the U.S. military launched strikes on Iranian missile sites, drone launch sites, and coastal radar stations. Despite this, oil remained under pressure because markets read the incident as a calculated tension, not the start of a full-scale escalation.

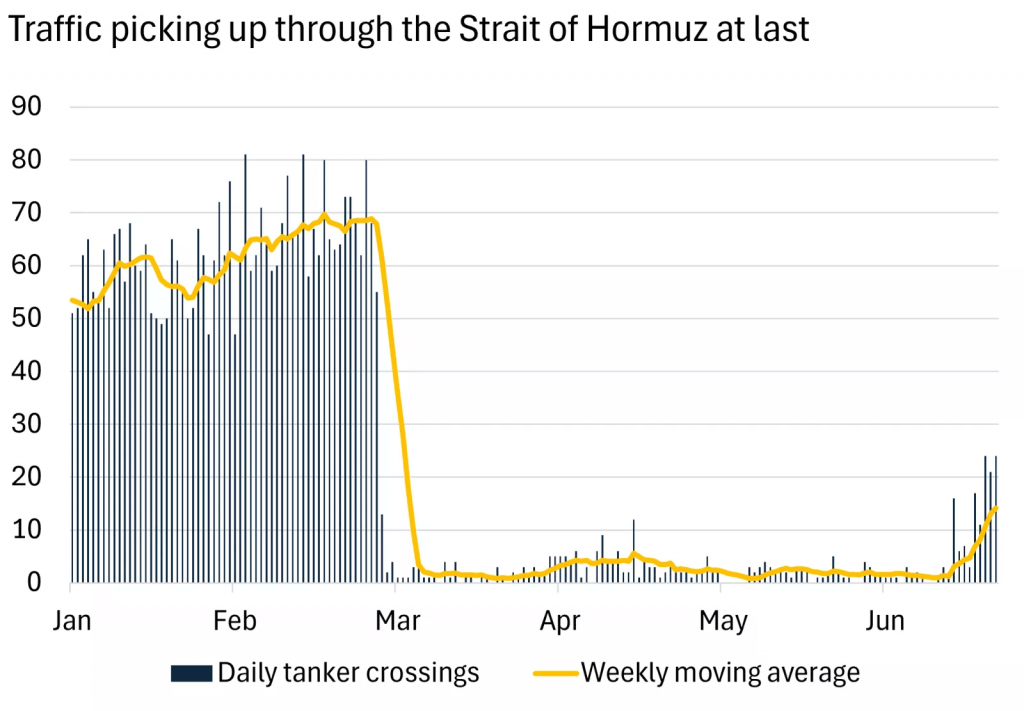

Oil ended the week with a bearish tilt, notably continuing to trade below the $70 per barrel level. Maritime data firm Windward confirmed that the Strait of Hormuz remains open with 43 commercial transits after the incident, but the pace of a return to normalcy clearly slowed, as the number was 78 transits on the busiest day this week, compared to a pre-war average of 130 or more daily.

Source: Bloomberg

IV. Gold — Trapped Between the Fed and the Dollar

At the start of the week, gold recovered part of its previous losses to trade at $4,197 an ounce, up $37, supported by diplomatic progress in Geneva and the drop in oil prices, which relatively eased inflation fears.

However, Fed pressure extinguished any attempts at sustained recovery. Thursday saw a slight recovery for gold after PCE data came in line with expectations, easing fears of an immediate interest rate hike and temporarily weakening the dollar. But the week ended with the yellow metal retreating to nearly $4,000 an ounce, recording weekly losses of about 5%, as hawkish signals from the Fed overwhelmed all geopolitical support.

It is worth noting that gold had reached its all-time high of nearly $5,000 in January 2026 at the peak of the Iranian crisis, and the current week solidified its cumulative decline of about 20% from those peaks, with the pressure of a strong dollar and high bond yields persisting.

V. The Dollar — Dominance Supported by Central Divergence

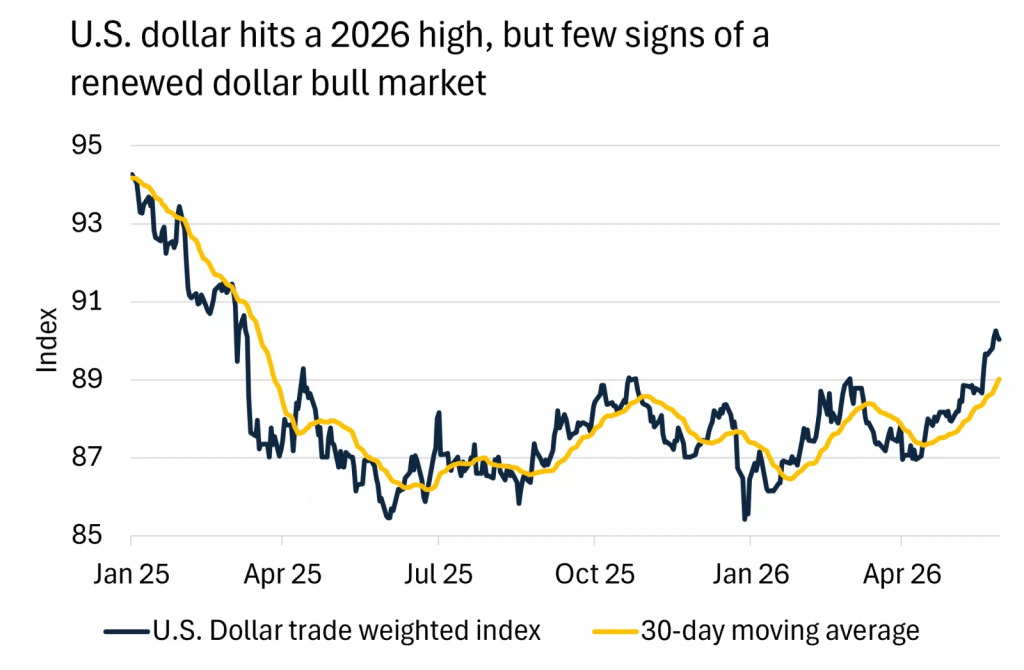

The dollar ended the week in limited volatility on Friday but recorded clear weekly gains against most major currencies, with the most notable gains against the Australian and New Zealand dollars.

Regarding the euro, the EUR/USD pair fell to about 1.1342 on June 25, recording its lowest level in over a year, while the DXY index crossed the 107.50 level, its highest level since November 2023. The main driver is the widening gap between the hawkish Fed and the dovish ECB.

Source: Bloomberg

The Japanese yen remains under historic weight; the USD/JPY pair tested the 161.95 level, a forty-year high, facing selling pressure from traders who found in this historic zone an opportunity for resistance. This level puts the Bank of Japan under increasing pressure to intervene, even if Japan’s loose monetary policy makes this option very costly.

VI. U.S. Treasury Bonds — A Curve Pricing the Tightening Era

By the end of the week, U.S. Treasury yields were drawn as follows: 3-month at 3.78%, 2-year at 4.13%, 5-year at 4.17%, 10-year at 4.4%, and 30-year at 4.86%. This upward-sloping curve reflects a genuine pricing of a world where interest rates are high for an extended period.

On Wednesday, 10-year yields fell below 4.5% as oil prices retreated, easing future inflation pressures. But on Friday, 2-year yields closed with a slight decline after Kashkari’s remarks, while energy declines contributed to easing pressure on short-term yields.

Source: BLS

VII. Fed Tone — The Hawkish Warsh Era Establishes Itself

The week lived in the complete shadow of the shift produced by the June meeting. In the June meeting, the Fed kept rates in the 3.50–3.75% range, but the real message was the shift toward tightening; previous indications of a potential rate cut were removed from the statement, and 9 out of 19 FOMC members supported a forecast for at least one rate hike during the year.

The Fed raised its 2026 core PCE inflation forecast from 2.7% to 3.3%, and does not expect to reach the 2% target before 2028 in the best estimates. Thursday’s PCE data reinforced these fears; the core inflation index rose to 3.4% in May, its highest level since October 2023, while headline inflation jumped to 4.1% annually.

Source: Fred

At the end of the week on Friday, Kashkari released a sharply hawkish tone, announcing his shift from expecting a rate cut to expecting one hike by the end of the year, warning that inflation pressures have become broader and have exceeded the impact of energy prices. In light of this, Bank of America changed its forecasts to adopt a scenario of three rate hikes of a quarter-point each during the year, which could raise the rate from the current range to 4.25–4.50%.

VIII. Geopolitics — The Strait of Hormuz Between Openness and Instability

The week’s geopolitical background cannot be understood without grasping the full context of the crisis. On June 14, Pakistani Prime Minister Shehbaz Sharif announced that the United States and Iran had signed a memorandum of understanding, followed immediately by Trump’s announcement of lifting the U.S. naval blockade on ships anchored in Iranian ports.

But within just eight days, the truce was violently shaken on Thursday, June 25, when the Iranian Revolutionary Guard launched an attack with four suicide drones on commercial ships in the strait, hitting a Singaporean ship in its upper section with structural damage but no casualties.

On Friday, Trump described the attack as a “foolish violation” of the agreement, indicating that his country’s forces shot down three drones. When asked about the consequences, he replied with his famous phrase, “You’ll find out.” Hours later, the U.S. military launched strikes on Iranian missile sites, drone launch sites, and coastal radar stations, in the most severe test yet of the temporary memorandum of understanding.

Conversely, the Iranian reaction was puzzling; the head of the National Security Committee in the Iranian Parliament announced that the strait is “under Iranian sovereignty, and the matter is not a violation of the truce, but rather management of the truce.”

Parallelly, British Prime Minister Keir Starmer announced his resignation on Monday, June 22, casting fleeting shadows over the British pound, which fell 0.19% against the dollar.

IX. Cryptocurrencies — Weekly Bleeding in the “Extreme Fear” Zone

The week was one of the harshest chapters for crypto in 2026. Bitcoin opened Monday at $63,242, down 1.6% from Sunday, while Ethereum opened at $1,704. On Thursday, Bitcoin collapsed below the $60,000 barrier to touch $59,334, its lowest level since 2024, while Ethereum fell to $1,561 during the session.

By the end of the week on Friday, Bitcoin opened at $59,706, a further 2.1% decline, while Ethereum fell 3.4% to $1,564. The bottom line of the figures: Bitcoin lost 5.6% during the week alone and 18.8% since the beginning of June, while Ethereum lost 8.2% during the week and 21.9% since the start of the month.

Regarding altcoins, XRP fell nearly 8% weekly, Cardano about 9%, and Dogecoin was the most painful with losses exceeding 9%. Conversely, Solana swam against the tide with weekly gains exceeding 7%.

Actual drivers were multiple and intertwined. Since May 15, U.S. spot Bitcoin ETFs recorded thirteen consecutive sessions of outflows, with a cumulative decline of about $4.4 billion. Thursday alone saw outflows from spot Bitcoin ETFs reach $696.3 million, while $81.9 million left Ethereum funds. The rise of the dollar and increasing expectations of interest rate hikes contributed to driving liquidity toward AI stocks instead of digital assets. Added to this is the potential delay of the CLARITY bill, which was counted on to resolve digital regulation. With the Fear and Greed Index dropping to 24 in the “Extreme Fear” zone, it seems the recovery phase will need a regulatory catalyst or a shift in the Fed’s stance.

X. Outlook for Next Week — A Decisive Agenda in a Shortened Week

Next week (June 29 – July 3) enters history as one of the most intense weeks due to the convergence of three threads: U.S. labor market data, the Central Bankers Summit in Sintra, and a constitutional ruling that may redraw the boundaries of the Fed’s independence.

Source: Bloomberg

Monday, June 29: The U.S. Supreme Court enters the final week of its current term, and its ruling is expected in the case of Trump’s firing of Fed board member Lisa Cook, a ruling that could consolidate or curtail the central bank’s margin of independence against the executive branch.

Tuesday, June 30: June U.S. consumer confidence data, the May JOLTS report, and the Chicago PMI are released. Eurozone preliminary inflation figures for June will also be published; these are critical data—with oil prices retreating about 20% during the month, they could produce a deflationary surprise that extinguishes talk of a July European rate hike.

Wednesday, July 1 — The Heaviest Day: The ECB Forum in Sintra, Portugal, kicks off under the theme “Shaping Europe’s Future: Innovation, Growth, and Stability.” In a historic moment, Fed Chair Kevin Warsh participates in an open discussion with ECB President Christine Lagarde, Bank of England Governor Andrew Bailey, and Bank of Canada Governor Tiff Macklem, in the first real test for Warsh before his global peers and his approach of refusing to provide forward guidance. On the same day, the ADP private employment report and the ISM manufacturing index for June will be released.

Thursday, July 2 — The Expected Report: The Bureau of Labor Statistics releases the U.S. jobs report for June a day early due to the Independence Day holiday. Expectations point to the addition of 172,000 jobs in June with the unemployment rate remaining steady at 4.3%. After average job growth in the last three months was about 188,000 jobs per month, markets will be highly sensitive: strong figures will solidify expectations of a September rate hike, and soft figures will give the Fed room to pause.

Friday, July 3: U.S. markets are closed for Independence Day.

Earnings-wise, Nike and Constellation Brands report on Tuesday, and General Mills on Wednesday.

Three Scenarios for a Highly Sensitive Week:

Scenario 1: A strong jobs report above 200,000 accompanied by a hawkish Warsh tone in Sintra — the September rate hike scenario becomes the rule, not the exception, and the dollar continues its rise while bonds, gold, and crypto remain under pressure.

Scenario 2: Soft figures below 120,000 accompanied by a tangible decline in Eurozone inflation — gives the Fed and the ECB room to pause, and allows markets to breathe.

Scenario 3: A Supreme Court ruling in favor of Trump in the Cook case — an extreme scenario that causes immediate disruption to the Fed’s credibility and fuels opportunistic gold buyers with further pressure on bonds.

What everyone shares is that this shortened week will be one of the most influential weeks in shaping the features of U.S. monetary policy for the second half of 2026, and what happens in just four trading days will determine whether markets will redraw their interest rate expectations upward to the point of certainty, or remain in the zone of open ambiguity that is difficult to plan for on any time horizon.