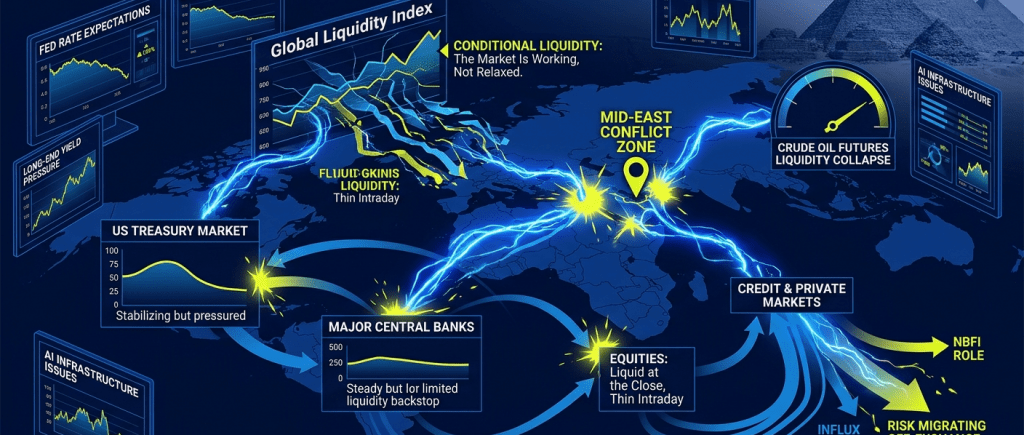

Conditional Liquidity: The Market Is Working, Not Relaxed

Global financial markets are still functioning smoothly on the surface, but liquidity is no longer broad-based. It is increasingly selective, concentrated in large-cap equities and core sovereign debt, while thinning out in risk assets, credit pockets, and commodity-linked markets.

The backdrop is shaped by four reinforcing forces: ongoing geopolitical tension in the Middle East, a cautious monetary policy stance from major central banks, structural changes in trading behavior, and rising leverage outside the traditional banking system.

The result is a market that clears efficiently in normal conditions, but becomes fragile quickly when stress appears.

Equities: Liquid at the Close, Thin in Between

Equity markets remain liquid overall, but the quality of that liquidity is changing.

A growing share of trading activity is now concentrated at the market close, where liquidity pools have deepened over time. This improves end-of-day price formation, but leaves intraday trading sessions comparatively thinner. The outcome is a dual structure: strong liquidity at a single point in time, weaker liquidity during continuous trading hours.

At the same time, extended and overnight trading sessions are expanding, largely driven by retail participation. These sessions, however, are structurally less liquid, with wider spreads and more volatile pricing behavior than standard trading hours.

This shift is reshaping how risk is absorbed: liquidity is no longer evenly distributed across the trading day, but compressed into specific windows.

U.S. Treasury Market: Stable Curve, Heavy Long-End Pressure

The U.S. government bond market remains the backbone of global liquidity, but it is showing clear structural stress at the long end.

The yield curve is upward sloping across maturities, with long-dated yields significantly higher than short-term rates. This reflects two key forces: persistent inflation uncertainty and continued heavy issuance of government debt.

Markets still broadly expect policy easing over time, but the path is no longer smooth. Any upside surprise in inflation data could quickly reprice the entire curve, particularly the long end where term premiums remain elevated.

In short, Treasuries are still liquid — but increasingly sensitive to macro shocks.

Monetary Policy: Quiet Support, Not Full Liquidity Expansion

Central banks are no longer in active crisis-response mode, but they continue to provide a stabilizing liquidity backstop.

Balance sheet operations focused on short-term government securities are helping maintain adequate reserves in money markets and smoothing short-term funding conditions. These actions are not equivalent to large-scale liquidity injections, but they prevent tighter financial conditions from feeding into disorderly market behavior.

At the same time, policymakers remain constrained by inflation risks tied to external shocks, particularly energy markets. This limits their willingness to provide aggressive liquidity expansion unless conditions deteriorate sharply.

Oil Markets: Liquidity Collapse and Volatility Spike

Energy markets stand out as the clearest example of liquidity stress.

Trading participation in crude oil futures has declined sharply amid geopolitical disruption in the Middle East. Market depth has thinned, open interest has dropped, and price swings have intensified as fewer participants are willing to absorb risk.

The physical disruption to supply routes has added another layer of instability, reinforcing volatility and discouraging hedging activity.

The result is a market where price discovery is still functioning, but with significantly reduced cushioning. Small shocks now produce outsized price reactions.

Credit and Private Markets: Risk Migrating Off-Exchange

Credit markets are undergoing a structural shift rather than a cyclical one.

Private credit continues to expand as a key funding channel for lower-rated borrowers, especially as refinancing needs build over the coming years. At the same time, traditional bond markets are absorbing large issuance waves tied to technology investment cycles, particularly in artificial intelligence infrastructure.

Non-bank financial institutions now play a much larger role in credit creation and leverage. This increases efficiency in normal conditions but raises concerns about transparency, funding stability, and liquidity during stress events.

The key feature is migration: risk is moving away from regulated bank balance sheets into less transparent parts of the financial system.

Japan: A Subtle but Important Liquidity Variable

In Japan, gradual adjustments to government bond purchase programs remain a quiet but important factor for global liquidity conditions.

The central debate centers on how quickly to reduce large-scale bond holdings without destabilizing long-end yields. A slower approach supports stability but risks prolonging distortions in price discovery, while faster normalization could introduce volatility into a market already sensitive to global rate shifts.

Given Japan’s size in global sovereign debt markets, even incremental policy changes have spillover effects on international liquidity flows.

Deep Markets, Narrow Safety Nets

Global liquidity in June 2026 is not scarce — but it is narrowly distributed.

Equities are liquid, but increasingly concentrated in specific trading windows

Sovereign bond markets remain functional, but sensitive to inflation and issuance dynamics

Energy markets are structurally impaired, with liquidity largely withdrawn

Credit is expanding, but increasingly routed through opaque non-bank channels

Central banks are stabilizing conditions, not expanding liquidity aggressively

The system still works efficiently under normal conditions. The risk lies in its reduced margin for error.

The key macro trigger ahead remains data on inflation and employment: these will determine whether markets continue to price a controlled policy path — or whether liquidity conditions tighten further through repricing rather than direct intervention.