The week of June 8–12, 2026, marks a pivotal juncture in the global economy, as markets transitioned from acute geopolitical panic to a phase of strategic anticipation and reassessment. Tensions in the Middle East—specifically the volatile trajectory of the U.S.–Iran negotiations—intersected with unexpectedly strong U.S. economic data, fueling uncertainty regarding global monetary policy trends. This report analyzes and comments on the developments of the week, reviewing the major variables that shaped the performance of financial assets.

The Geopolitical Landscape: From Escalation to Cautious De-escalation

The week began under the weight of fears regarding the escalating Iran–Israel conflict, which pushed oil prices near $96 per barrel in Monday’s opening session, driven by concerns over supply chain disruptions in the Strait of Hormuz. However, mid-week saw a dramatic turnaround following reports of a 14-point draft agreement being studied by the U.S. administration and Tehran, aimed at de-escalation.

This geopolitical shift became the decisive factor in “repricing” risk in the markets. Brent crude fell by more than 4% within a few days, closing the week near $86.5, reflecting cautious optimism that easing tensions could lead to additional oil flows and mitigate inflationary pressures. Nevertheless, markets remain cognizant of the fragility of this agreement; any setback in negotiations could trigger a rapid rebound in energy prices, keeping investors in a state of constant vigilance.

US Economic Data: The Dilemma of Resilience and Inflation

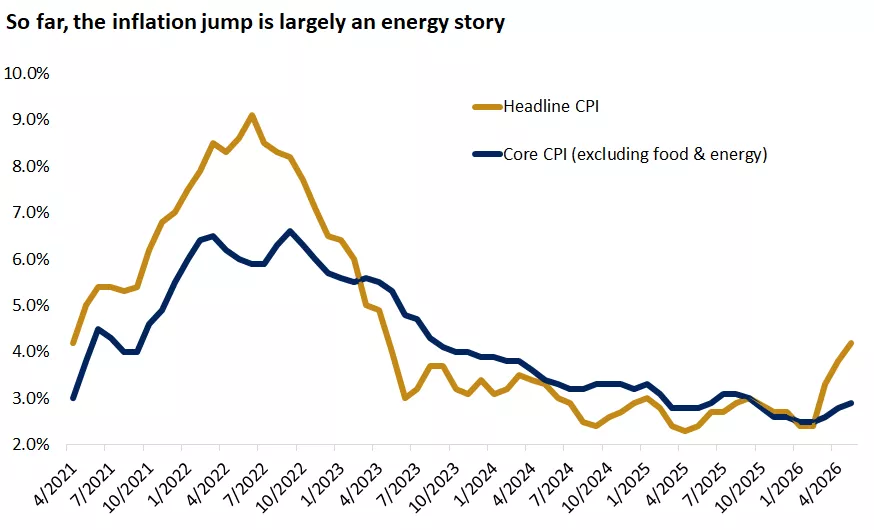

U.S. economic readings for May 2026 added complexity to the scene. The economy added 172,000 jobs, significantly exceeding analysts’ expectations of just 85,000. This resilience in the labor market, despite tight monetary policies, sends a dual signal:

Source: Bloomberg

On one hand, it is proof of economic strength and the avoidance of recession; on the other, it provides the Federal Reserve with greater latitude to continue aggressive policies to combat inflation, which recorded 4.2% annually. The rise in the Consumer Price Index to this level, driven by energy prices, places “Kevin Warsh,” the new Fed Chair, before a complex challenge. Inflation stemming from geopolitical factors is difficult to curb with traditional interest rate tools without risking a growth slowdown. This situation, economically known as potential stagflation, explains why markets remain in a state of “cautious optimism.”

Market Performance: Equity Resilience and Tech Correction

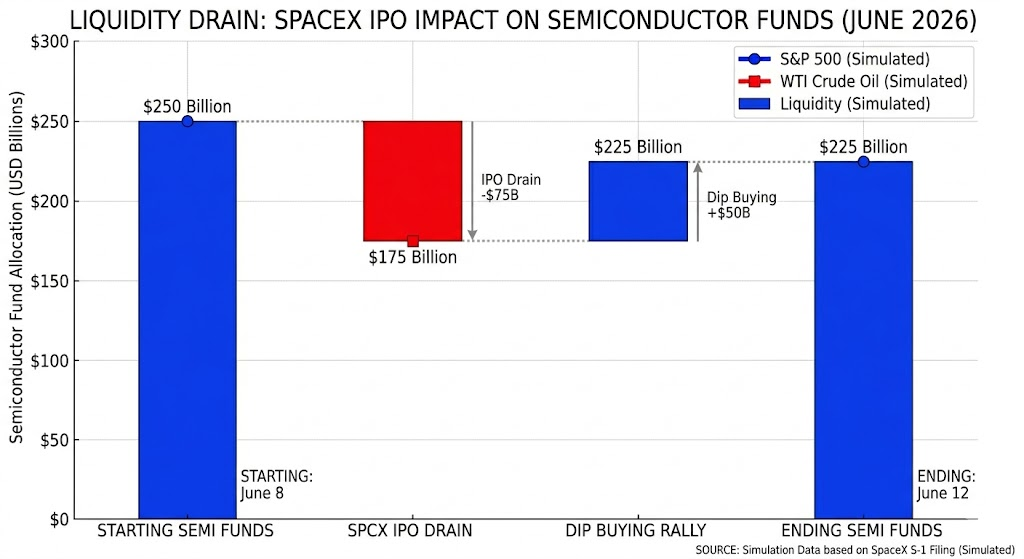

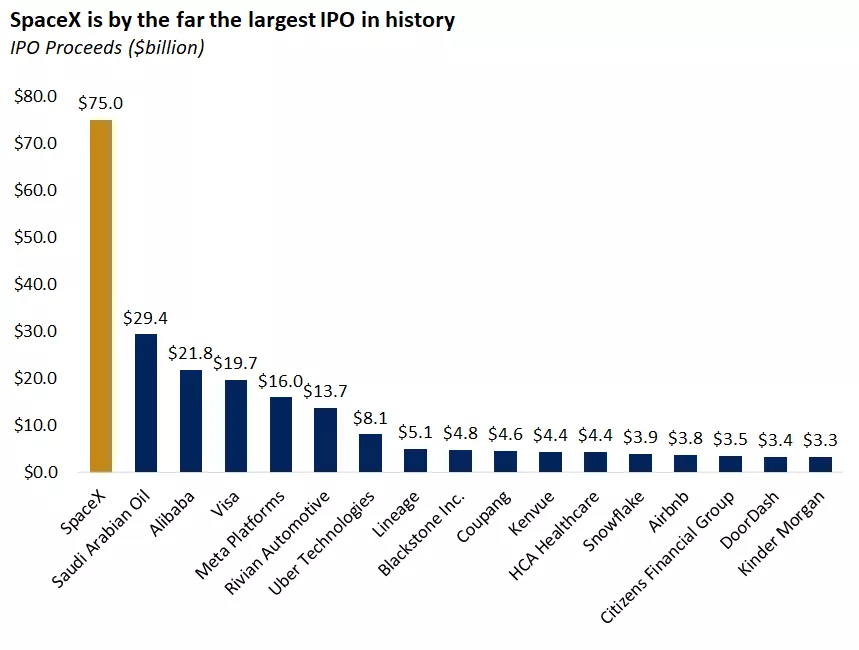

U.S. stock indices witnessed sharp fluctuations, with the Nasdaq dropping by approximately 7% from its peak before paring losses in the end-of-week sessions. This correction was not driven by weakness in companies’ operational fundamentals, but rather by a “structural liquidity shortage” associated with “IPO liquidity.” The listing of SpaceX (SPCX), the largest IPO in history, raising $75 billion, triggered a massive “Liquidity Drain.” Major institutional funds and hedge funds were forced to liquidate profitable positions in tech giants, such as Nvidia and semiconductor firms, to free up the cash required to participate in the new offering—a practice known in financial markets as “Capital Reallocation.”

Prepared By Noor Trends Team

This sudden surge in liquidity toward the IPO exacerbated uncertainty, which was clearly reflected in the Volatility Index (VIX). The VIX jumped from relatively calm levels to the 22-point zone mid-week, reflecting higher “risk premiums” among traders. When the VIX rises this sharply, algorithmic trading systems trigger “automatic sell” orders as soon as critical moving averages are breached, compounding the severity of the decline in the semiconductor sector. The sell-off was not based on corporate valuations but was mainly driven by “Margin Calls” and position hedging.

However, the market demonstrated structural resilience. Once the IPO wave was absorbed and liquidity pressures receded, the VIX retreated toward stability, prompting “Dip Buyers” to return forcefully. This end-of-week consolidation confirms that previous gains were not a bubble, but were supported by real cash flows betting on AI. The market proved that demand for technical infrastructure remains the “underlying engine” of market capitalization, and that any dip in liquidity is not a shift in the overall market trend. What occurred was a liquidity “Stress Test,” proving that markets still possess enough cash reserves to re-enter upon the conclusion of massive multi-billion-dollar IPOs.

The Global Monetary System: The ECB and the Yen

The European Central Bank took a significant step by raising interest rates by 25 basis points to 2.25%, a move aimed at containing inflationary pressures that have begun to seep into the Eurozone economy. This decision narrowed the interest rate gap with the U.S. dollar, providing slight support to the Euro. Conversely, all eyes remain on the Bank of Japan; the USD/JPY pair surpassed the 160 level—a sensitive threshold that concerns monetary authorities. The Japanese Yen is not merely a currency; it is the global engine for funding “Carry Trade” positions (borrowing at low interest rates to invest in high-yield assets).

It is worth noting that any signal of tightening from the Bank of Japan in its upcoming meeting will lead to a sudden withdrawal of liquidity from global markets, making the monitoring of this pair a strategic necessity for any investor this week.

Cryptocurrencies and Gold: Contradiction and Hedging

Gold prices showed resilience despite strong economic data, stabilizing around $4,200 per ounce. Although gold is typically negatively affected by rising bond yields, investors have begun to view it as a hedge against potential “monetary failure.” As for Bitcoin, it witnessed a strong rebound to the $63,800 level, driven by positive inflows into ETFs.

What is notable here is the correlation beginning to form between cryptocurrencies and major tech stocks. Since SpaceX holds massive Bitcoin portfolios, Bitcoin’s price is now indirectly influenced by major institutional decisions, shifting its speculative nature from an “alternative asset” to an “institutional asset” sensitive to market volatility.

Source: Factset

Outlook for the Coming Week

Investors enter this week in a state of maximum anticipation, as the features of U.S. monetary policy will be defined by the Federal Open Market Committee (FOMC) meeting. Expectations point toward a wait-and-see bias, with a focus on “Kevin Warsh’s” tone. The importance of this meeting lies less in the rate decision itself and more in the “Forward Guidance.” If the Fed signals that inflation has peaked, we will witness a strong rally in stocks and bonds. On the other hand, geopolitical risks remain a “wild card”; a failure in de-escalation negotiations would completely flip the table and drive energy prices back up, forcing central banks to adopt more aggressive stances.

The current week remains a transitional period, necessitating an “liquidity management” strategy rather than reckless expansion of positions. Furthermore, the stabilization of 10-year bond yields at 4.48% provides a degree of stability, though the volatility potentially imposed by the Bank of Japan’s decision persists.

Diversification between real assets, such as precious metals, and maintaining sufficient cash levels remains the wisest choice in this volatile environment, which is testing the global economy’s ability to adapt to high inflation and a constantly changing geopolitical reality. Markets in 2026 do not need optimistic or pessimistic forecasts, but rather careful monitoring of the digital facts reflected by central bank decisions and the movements of institutional liquidity.