The US dollar showed mixed performance over the past week, starting on a weak note as sentiment improved amid diplomatic efforts in the Middle East, before regaining strength later, supported by a combination of positive economic data, escalating geopolitical tensions, and rising oil prices. This is reflected, along with other developments across financial markets, in the weekly summary.

At the beginning of the week, remarks by US President Donald Trump about nearing an agreement to end the war with Iran weighed on the US currency. These statements boosted optimism and led to a decline in the dollar amid improved risk appetite.

The announcement of a ceasefire agreement between Israel and Lebanon, mediated by the United States, also supported positive sentiment. However, this did not fully dispel concerns, particularly as investors remain aware that negotiations between Washington and Tehran often fluctuate between optimism and disappointment.

The situation quickly shifted after Iran announced it was halting ceasefire talks with the United States, raising fears of a broad military confrontation. This development restored demand for the dollar as a safe haven and pushed it to strong gains, alongside a rise in oil prices by more than 7.00%. This was directly reflected in US Treasury yields and widened the interest rate differential in favour of the US currency.

On the economic front, the ADP employment report showed the addition of 122,000 new jobs in May, exceeding expectations. Meanwhile, the services PMI rose to 54.5, and factory orders recorded their largest increase in 11 months at 4.8%.

These figures reinforced confidence in the resilience of the US economy, despite weekly jobless claims rising to 225,000, indicating some slowdown in the labour market without pointing to a severe downturn.

The manufacturing PMI rose to 54.0, while the final manufacturing reading edged slightly lower to 55.1. At the same time, the input prices index declined to 82.1, reflecting easing inflationary pressures, a positive factor for markets.

In terms of monetary policy, markets priced in a 95% probability that the Federal Reserve would not raise interest rates at its mid-June meeting, limiting expectations for further tightening.

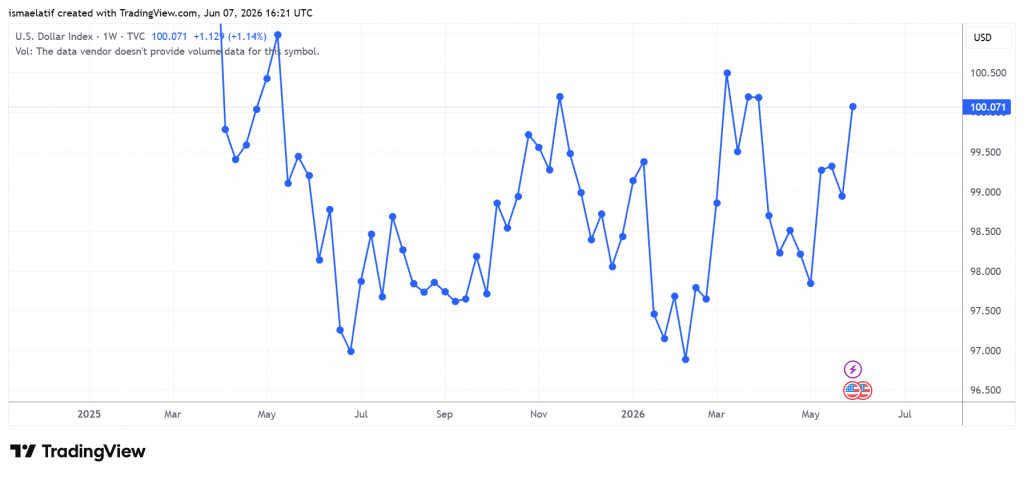

Nevertheless, the combination of positive data and geopolitical tensions kept the dollar in a strong position by the end of the week, with the dollar index rising by around 0.5%, supported by safe-haven demand and higher oil prices.

In currency markets, the dollar was the weakest at the start of the week, followed by the Canadian dollar and the Japanese yen, while the Swiss franc, euro, and British pound led gains.

By the end of the week, the dollar regained its position, supported by economic and geopolitical factors, reflecting a volatile but ultimately strong trajectory overall.

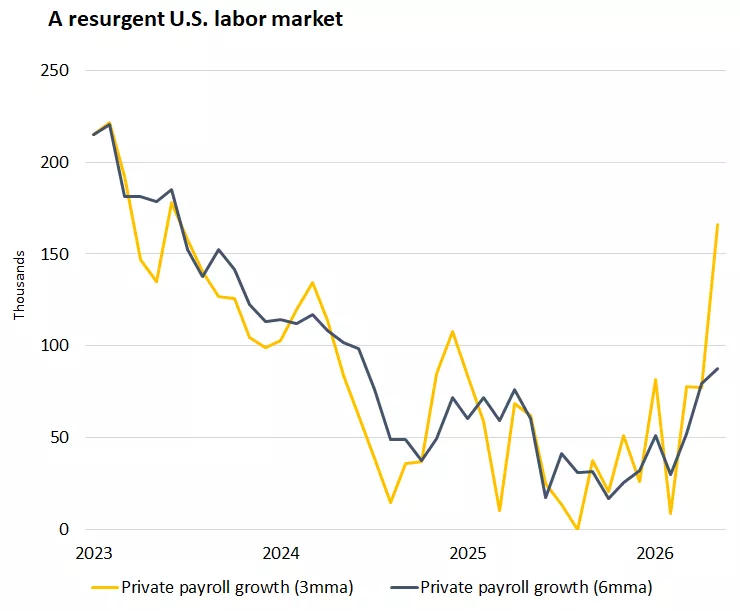

The US labour market demonstrated notable resilience, with employers adding 172,000 jobs in May, exceeding expectations, despite economic challenges linked to rising costs stemming from the war with Iran.

According to US Department of Labor data, this figure was slightly below the revised April figure of 179,000, indicating a modest slowdown in hiring but still reflecting relatively stable labour market performance. The unemployment rate remained steady at a relatively low 4.3%.

This performance comes amid a gradual recovery in the labour market during 2026, following a period described as difficult in 2025. The market has been able to absorb the effects of higher energy prices and economic uncertainty following the strikes carried out by the United States and Israel on Iran in late February.

The US dollar rose at the close of Friday trading, supported by growing expectations that the Federal Reserve will keep interest rates unchanged at elevated levels in the near term, following the positive picture painted by labour market data in the United States.

Weekly gains for the greenback – Source: tradingview

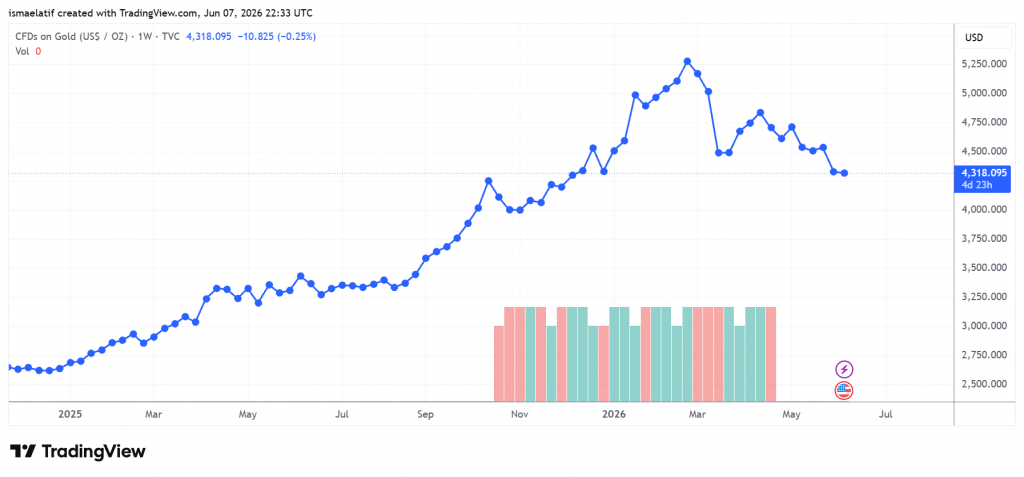

Gold Between Pressure and Recovery

The precious metal experienced a volatile week, starting with a sharp decline on Monday of around $85.30 per ounce, or 1.9%, before continuing to fall midweek under the influence of various economic and monetary factors, then rebounding toward the end of the week with notable gains, supported by a weaker dollar and declining oil prices.

At the start of the week, the strength of the US dollar pressured gold, as a stronger currency reduced the appeal of the metal, which is priced in dollars, making it more expensive for holders of other currencies.

Higher global bond yields also contributed to increasing the opportunity cost of holding gold, a non-yielding asset, prompting investors to reduce their positions.

Statements by Bank of Japan Governor Kazuo Ueda regarding the risks of elevated inflation also contributed to gold’s decline, as expectations grew for tighter global monetary policies.

US economic data added further pressure, with the ADP employment report for May coming in stronger than expected, alongside a rise in the services PMI and improved industrial orders.

These readings strengthened bets on the continuation of the Federal Reserve’s hawkish approach, negatively impacting gold prices.

Key labour market data reinforced continued improvement in US employment conditions.

Other factors also weighed on gold, notably the liquidation of long positions in the metal within exchange-traded funds, with holdings falling to their lowest level in five and a half months at the end of March, after reaching a three-and-a-half-year high in February.

However, demand for gold from central banks remains on the rise, led by the People’s Bank of China, which increased its reserves by 260,000 ounces in April to reach 74.64 million ounces, marking the largest monthly increase in a full year and the eighteenth consecutive month of increases.

This support was not sufficient amid prevailing downward pressures, resulting in weekly losses of more than 4.00%.

Pressured by the dollar

Geopolitical Tensions Weigh on Equities

Global markets have experienced heightened tension recently, with stocks coming under clear pressure alongside rising oil prices, following reports that Iran had halted ceasefire negotiations, reviving concerns about the stability of global oil supplies.

This development highlights the sensitivity of markets to any changes in the geopolitical landscape, particularly in the Gulf region, a critical artery for global energy supplies.

Equity markets also faced selling pressure, as investors tend in such conditions to reduce risk exposure and shift away from more volatile assets toward safer ones.

Rising oil prices have become the primary driver of market movements at present, increasing production and transport costs, pressuring profit margins, and limiting consumer purchasing power.

On the other hand, strong spending on artificial intelligence supported technology stocks, with Hewlett Packard Enterprise and Marvell Technology shares rising by more than 24% on optimistic growth expectations.

However, negative factors limited gains, notably weakness in software stocks and a 4% decline in Bitcoin, which weighed on crypto-related equities.

Markets also faced additional pressure from rising US Treasury yields, with the 10-year yield reaching 4.46%, negatively affecting equity valuations, particularly in the interest rate-sensitive technology sector.

The US labour market showed notable resilience, with employers adding 172,000 jobs in May, exceeding expectations, despite economic challenges related to rising costs stemming from the war with Iran.

According to US Department of Labor data, this figure was slightly below the revised April figure of 179,000, signalling a modest slowdown in hiring while still reflecting relatively stable labour market performance. The unemployment rate remained steady at 4.3%, reinforcing expectations that the Federal Reserve will avoid cutting interest rates in the near term, which in turn weighed on global equities.

Source: FRED

External Pressures and Limited Internal Support for the Euro

The euro recorded a volatile performance during the week, characterised by opposing forces, as it came under clear pressure at the beginning before attempting a limited recovery supported by European economic data. These movements reflect cautious balance in the markets between negative and positive factors affecting the single currency.

At the start of the week, the euro declined noticeably against the US dollar, with the EUR/USD pair falling by around 0.4% during Monday trading. This decline was driven by the strength of the dollar and increased demand for it as a safe haven, alongside rising geopolitical concerns linked to tensions between the United States and Iran. This reduced investor risk appetite, putting pressure on growth-sensitive currencies such as the euro.

Rising oil prices also weakened the euro, given the eurozone economy’s heavy reliance on energy imports. This increased economic costs and negatively impacted growth expectations, weighing on the currency.

Despite these pressures, the euro gained some support from positive economic data. Manufacturing PMI data showed a slight improvement, rising to 51.6, indicating a relative recovery in industrial activity.

Additionally, expectations that the European Central Bank would raise interest rates by 25 basis points at its upcoming meeting strengthened significantly, nearing consensus, supported by inflation data, particularly core inflation and rising services prices.

During Tuesday trading, these positive factors contributed to a slight rise in the euro against the dollar, although limited to less than 0.1%, reflecting continued balance as persistent pressures from a strong dollar and higher oil prices constrained further gains.

Meanwhile, inflation in the eurozone remained elevated, with the annual rate at 3.2% and core inflation rising to 2.5%. These levels supported expectations of monetary tightening, providing additional support for the euro, though not sufficient to decisively change the overall direction.

Overall, the euro’s performance during the week can be described as range-bound, starting with clear losses followed by a partial recovery supported by economic data and interest rate expectations, while external pressures, particularly dollar strength and rising energy prices, maintained a climate of uncertainty.

Weekly Losses for Oil

Oil prices experienced sharp fluctuations during the past week, driven by escalating geopolitical tensions between the United States and Iran and the continued closure of the Strait of Hormuz, a vital artery for global energy supplies.

West Texas Intermediate crude rose strongly at the beginning of the week, supported by Iran suspending communication with Washington regarding a ceasefire agreement, raising widespread concerns about supply disruptions.

Prices continued to rise on Tuesday by 4.1% to reach $96.20, driven by statements from US President Donald Trump casting doubt on the continuation of the ceasefire, describing the agreement as “on life support”.

Despite these fluctuations, the overall direction of prices reflects deep concern in global markets, as geopolitical factors intersect with supply and demand fundamentals.

With the ongoing war and stalled negotiations, the market remains in a state of severe supply tightness, making any political or field development capable of rapidly and sharply changing price direction.

Oil ended the week lower, as investors priced in the possibility of a peace agreement between the United States and Iran in the near term.

The New Week: Focus on Inflation and the “Magnificent Seven”

Global markets enter a busy week of economic events, led by the release of consumer price index data, alongside key updates from major technology companies, at a time when investor sensitivity to inflation and its implications for monetary policy is increasing.

Inflation data is expected to be the main focus, with the May CPI reading due on Wednesday. The report follows April data showing an annual increase of 3.8%, the highest level in nearly three years, largely driven by rising energy prices, particularly fuel, which increased by more than 28%.

Core inflation, which excludes the more volatile food and energy prices, rose by 2.8% year-on-year, indicating that inflationary pressures are spreading beyond energy into other sectors of the economy.

Investors are also watching other data, including the producer price index, which rose by 6.00% year-on-year in April, and the personal consumption expenditures index, which also recorded an annual increase of 3.8%, reflecting continued price pressures across the economy.

On the corporate front, attention is turning to the technology sector, with key updates and earnings expected from major companies. Adobe is set to report its results, while Apple is expected to unveil new technologies and products at upcoming events, highlighting innovation trends in the sector.

The potential initial public offering of SpaceX is also a focal point, with expectations that it could bring the company’s valuation to $1.75 trillion, with the possibility of other listings to follow.