Geopolitical developments continued to dominate headlines throughout the past week, yet global financial markets gradually shifted their focus back toward economic data and corporate earnings — a dynamic explored in this week’s summary. This shift helped propel U.S. equity indices to new record highs, at a time when economic indicators suggest that the U.S. economy remains on solid footing despite persistent uncertainty surrounding the Middle East conflict and rising energy prices.

Against this backdrop, the interplay between two major forces — the war in the Middle East and the optimism sparked by strong U.S. employment data — has created a highly complex market environment. Global financial assets are responding to conflicting signals: improving labor‑market conditions and strong corporate earnings on one hand, and escalating geopolitical risks on the other.

Growing Hopes for a Peace Agreement with Iran

The conflict in the Middle East remains at the forefront of global attention, but recent developments have injected a dose of optimism into markets. The most notable event last week was the unveiling of a U.S. proposal to end the war — a one‑page document that, according to Axios, includes 14 provisions, among them:

- A temporary halt to Iran’s uranium enrichment program

- The lifting of U.S. sanctions

- The removal of restrictions on traffic through the Strait of Hormuz

The report described the proposal as “the closest the two sides have come to an agreement since the war began.” This optimism was immediately reflected in markets, with U.S. equity indices hitting fresh record highs.

Although markets are still awaiting Iran’s official response, “signs of progress in the talks” have strengthened expectations that a diplomatic solution is possible, even as tensions in the Gulf remain elevated.

Markets Re‑Engage with Economic Data

Despite the ongoing conflict, markets have increasingly refocused on core economic fundamentals rather than day‑to‑day oil price swings. This shift has produced several distinct market trajectories.

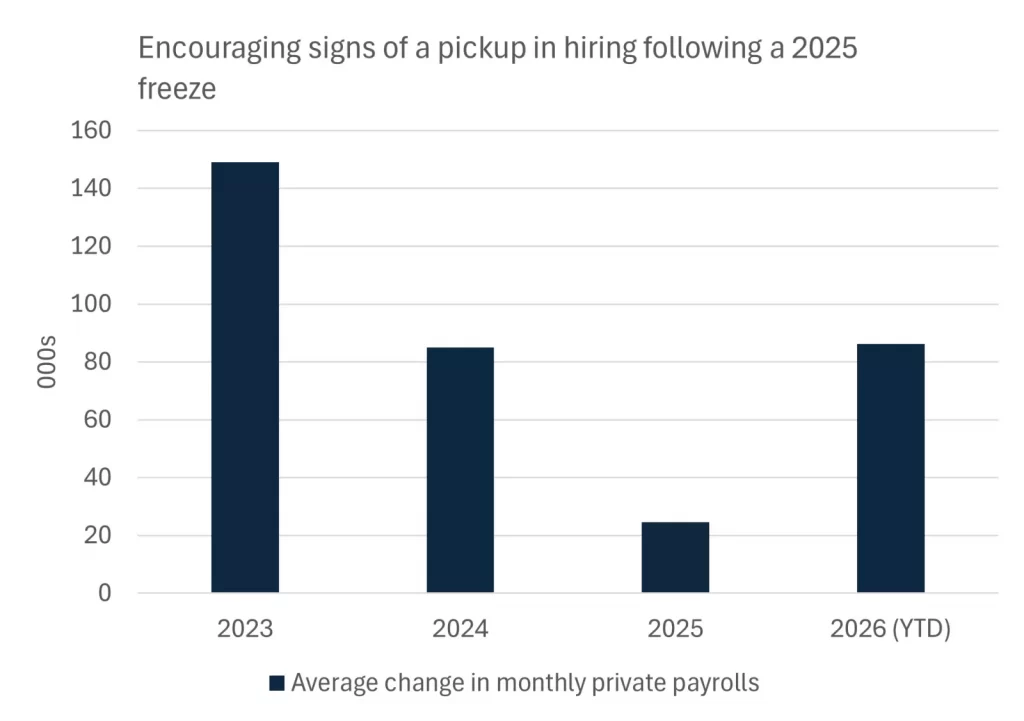

The U.S. economy entered 2026 amid concerns about a cooling labor market. Private‑sector job growth averaged just 25,000 jobs per month in 2025, while unemployment rose from 4.1% to 4.5%. Although there were no signs of collapse, weak hiring was flagged by the Federal Reserve as a potential risk.

However, April’s data painted a very different picture, highlighting a sharp improvement in labor‑market conditions. Payrolls posted back‑to‑back increases in March and April for the first time in a year, lifting average private‑sector job growth to 90,000 jobs per month so far in 2026. Unemployment has also retreated from its 2025 peak, stabilizing at 4.3% in April.

The improvement has been broad‑based. The payroll diffusion index — which compares the number of sectors adding jobs versus those cutting them — has risen significantly over the past six months, indicating that hiring strength is spread across a wider range of industries.

Additional indicators reinforce this trend:

- A decline in unemployment‑benefit claims

- Improved household perceptions of job availability

- A rise in the hiring rate for unemployed workers, according to the Chicago Fed

These signals suggest that the U.S. labour market remains resilient even in the early stages of an energy‑price shock. Still, there are concerns that a prolonged rise in oil prices could threaten this momentum.

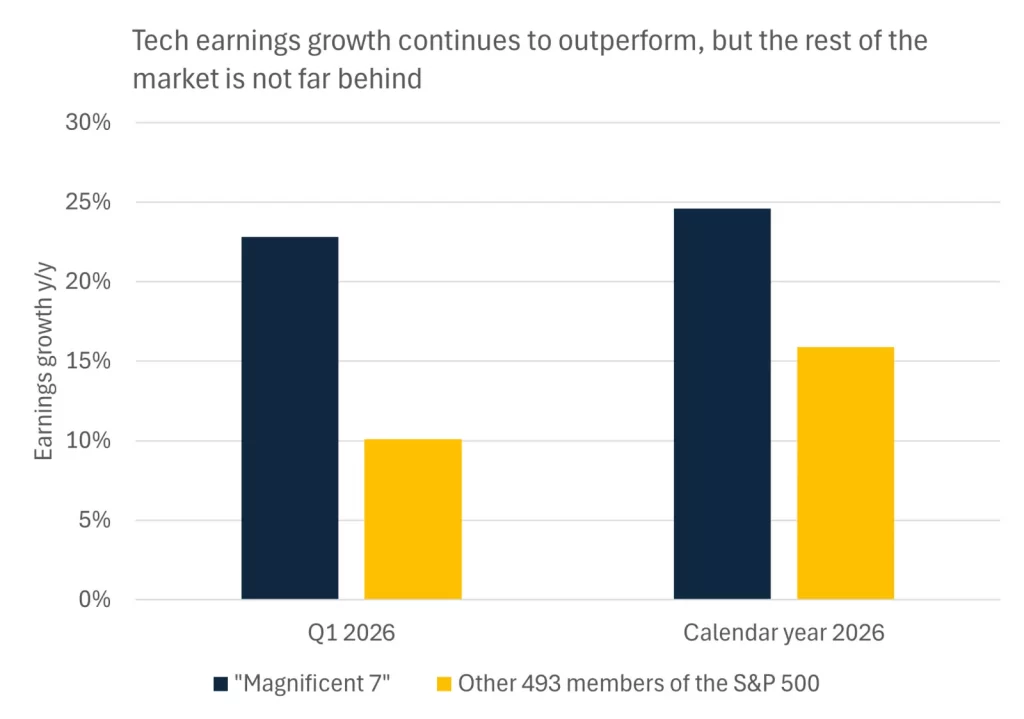

Technology Leads an Exceptional Earnings Season

Rising oil prices have not been the main story in recent corporate earnings. Instead, the dominant theme has been broad‑based earnings strength, with standout performance from technology and AI‑related companies.

As the first‑quarter earnings season nears completion, the numbers show:

- 89% of S&P 500 companies have reported

- 84% have exceeded earnings expectations

- Blended earnings growth is approaching 28%, the strongest since 2021

- 10 of 11 sectors have posted positive year‑over‑year earnings growth

- 7 sectors have delivered double‑digit gains

These results highlight the strength of corporate profitability heading into the oil‑price shock, suggesting that companies are well‑positioned unless energy prices rise significantly further.

The technology sector has been the standout performer, fueled by an extraordinary investment cycle in artificial intelligence. The Philadelphia Semiconductor Index surged more than 10% last week alone and is now up 65% year‑to‑date.

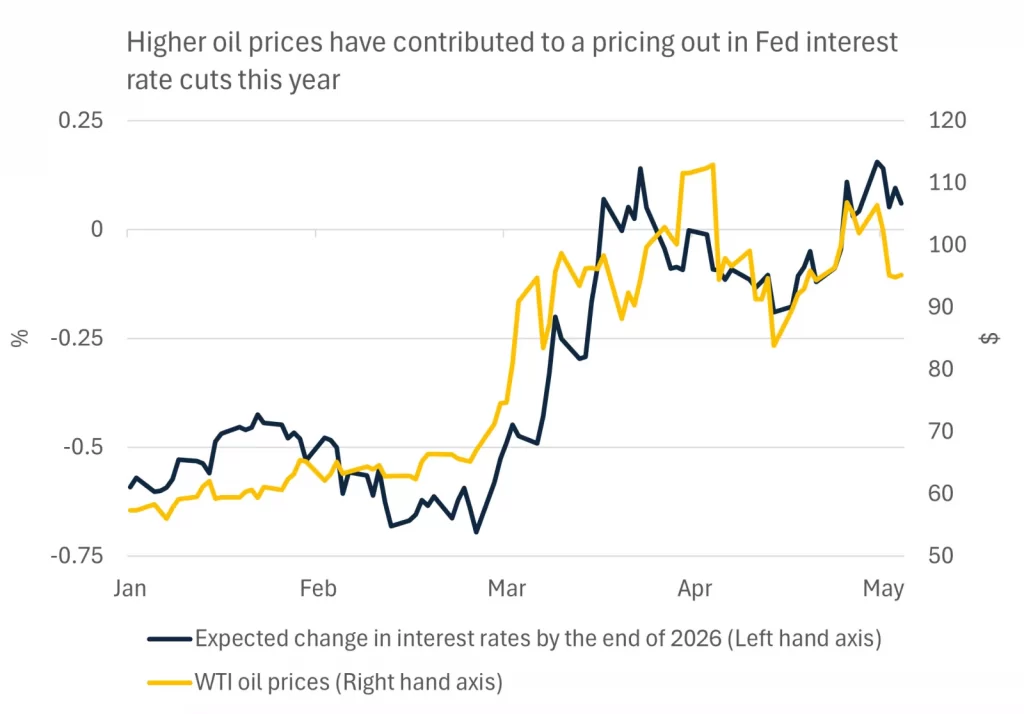

Markets Reprice the Federal Reserve’s Policy Path

The combination of stronger labour‑market data and robust earnings has prompted investors to reassess the Federal Reserve’s policy outlook.

While equities have fully recovered from the Middle East shock, the bond market has not. The yield on the 10‑year U.S. Treasury has climbed to 4.36%, up 40 basis points from its February low. This reflects a sharp decline in expectations for rate cuts. Before the Iran shock, markets were pricing in two cuts this year; now, expectations suggest the Fed may not cut rates anytime soon.

Three key factors explain this shift:

- Inflation has risen to 3.3%, with expectations of a further increase in April before easing later in 2026. Even if temporary, higher inflation complicates rate‑cut decisions.

- Improved labour‑market conditions and economic resilience reduce the urgency for policy easing. With strong profits and solid hiring, the Fed sees little need to rush into cuts.

- A more hawkish tone within the FOMC, reflected in recent dissents over guidance suggesting the next move would be a cut. This internal division makes it harder for incoming Chair Kevin Warsh to build consensus for near‑term easing.

The Fed is expected to hold rates steady for the next several meetings, with the possibility of a single cut by year‑end if oil prices and inflation moderate.

The Week Ahead

Financial markets are now awaiting fresh inflation data and indicators of consumer spending. Key releases include:

- The April Consumer Price Index (CPI)

- Retail sales data

- Reports on industrial production and consumer sentiment

These indicators will help determine whether the economy is slowing or maintaining steady growth. Meanwhile, earnings season continues, with major retailers set to report results that will offer insight into consumer demand in a high‑price environment.

As investors await these releases, monetary‑policy expectations remain central. Any surprise in inflation or spending could reshape the outlook for rate cuts in the coming months.