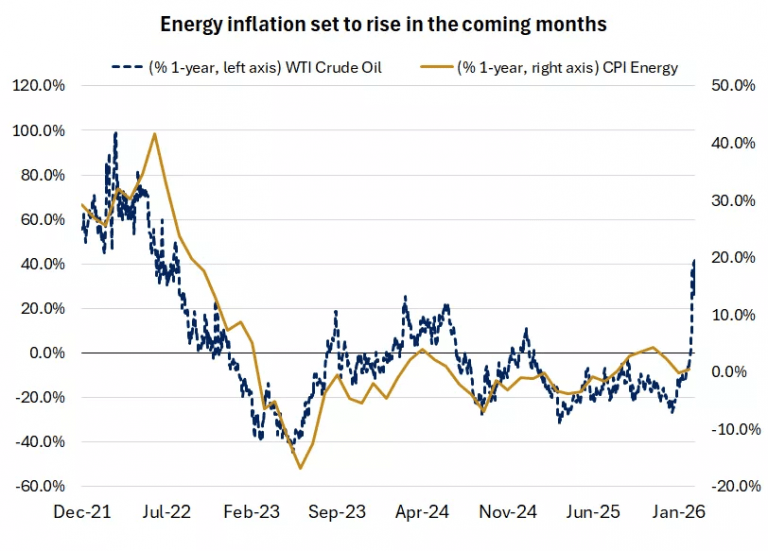

Recent disruptions in global oil supplies, stemming from the conflict in the Middle East, drove prices to elevated levels last week, sparking a wave of volatility in financial markets across key asset classes. While global equity markets ended the past week lower, Treasury yields saw a significant rise. Despite recent inflation data suggesting a gradual easing of price pressures, the latest spike in energy prices warns of renewed upward pressures on the horizon. This presents monetary policymakers with a complex landscape ahead of the highly anticipated Federal Reserve meeting this week.

Oil Volatility: Temporary Headwinds?

Despite these challenges, analysts believe the current rise in oil prices represents temporary “headwinds” that may delay the path of interest rate cuts but will not ultimately derail it. The global economy entered this phase with strong positive momentum, supported by low unemployment rates and solid growth in global earnings—expected to reach 15% for S&P 500 companies and 17% for international firms in 2026.

Source: World Bank

Resilience of the U.S. Economy

The structure of the U.S. economy has likely become more resilient to energy shocks, thanks to the United States’ transition into a net energy exporter and the increased share of the service sector in the Gross Domestic Product (GDP).

Drawing from Strategic Petroleum Reserves

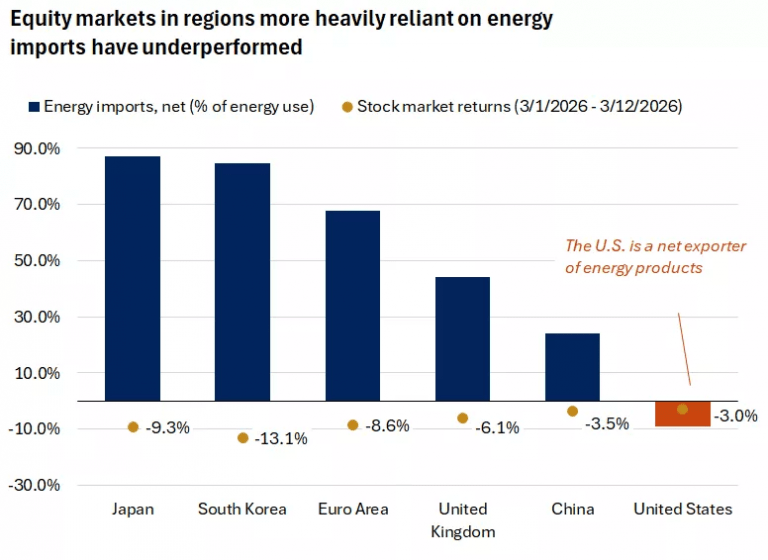

On the international market front, the decline was more pronounced in Europe and Asia due to their heavy reliance on imported energy. Markets in Japan, South Korea, and the Eurozone recorded drops exceeding 8% since the start of the conflict. Parallel to this, a 2.5% rise in the Dollar during March pressured investment returns outside the U.S. As oil continues to trade at levels roughly 45% higher than pre-conflict prices, markets are monitoring the effectiveness of international measures—such as the withdrawal of 400 million barrels from strategic reserves—to restore price stability toward the 2025 average of $65 per barrel.

Amidst this volatile scene, strategic optimism remains for the long-term outlook. Current pullbacks provide attractive entry points for investors, particularly in large and mid-cap U.S. stocks driven by AI investments, as well as small-cap stocks in developed and emerging markets. Maintaining a diversified investment strategy aligned with long-term financial goals remains the optimal choice, rather than being swayed by momentary reactions to headlines.

Markets Bet on a New Bullish Wave for the Greenback

Global financial markets are witnessing a clear shift in trends as geopolitical tensions escalate and energy prices rise. The U.S. Dollar continues to consolidate its gains, driven by its traditional role as a safe haven during crises. With the ongoing war in Iran and the accompanying disruptions in oil and shipping markets, investor bets are increasing on the possibility of the U.S. currency reaching even higher levels through 2026.

Dollar Momentum Returns with Force

The Dollar Index (DXY) saw a notable rise to nearly 100 points, heading toward its strongest close in over three months. This performance follows a wave of broad volatility in global markets that pushed investors toward safer assets, bringing the Dollar back to the forefront as a preferred defensive option.

Conversely, other major currencies faced clear pressure. The Euro fell to its lowest levels in several months, while the Japanese Yen approached its weakest level in nearly twenty months, prompting Japanese authorities to issue warnings regarding potential market intervention to protect their currency.

Betting on Continued Upside

Movements in the financial options markets reflect increasing bets on a Dollar rally in the coming period. Demand for “call options” on the U.S. currency against “puts” rose to its highest level since late 2022, signaling strong expectations for continued Dollar strength under current geopolitical conditions. This coincides with a sharp rise in oil prices, with Brent crude surpassing $100 per barrel again.

Oil and Inflation Redraw the Path of Interest Rates

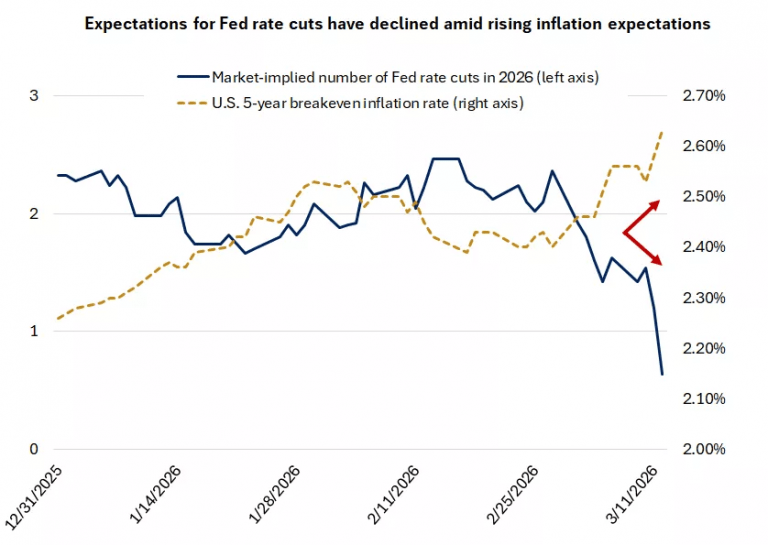

Rising energy prices are stoking fears of a return of inflationary pressures in the U.S. economy, which could complicate the interest rate cut plans investors were expecting this year. Experts suggest Brent crude could hover around $98 per barrel through March and April before gradually receding. However, this temporary high could be enough to push inflation upward, potentially delaying the first U.S. rate cut from mid-year to a later date. This scenario typically supports Dollar strength, as sustained high U.S. rates attract more investment into Dollar-denominated assets.

Markets Await Powell: Will the Fed Hint at a Surprise?

The world’s eyes are on the Federal Reserve’s March meeting, with expectations that Chairman Jerome Powell’s remarks will carry vital signals about the future of monetary policy. This meeting comes as fears rise of a “stagflationary” mix—slowing growth combined with high inflation—following the massive jump in global oil prices.

Source: FactSet

A Policy of “Wait and See”

Despite inflationary pressures, the Fed is expected to keep rates unchanged in its upcoming meeting. The central bank appears to prefer monitoring economic developments closely before taking any new steps. Economists see a likely scenario of a limited rate cut this year, followed by another next year, placing the terminal rate in the 3.00% to 3.25% range.

Source: FactSet

Gold Between Rates and Geopolitical Tensions

The Fed’s decision is particularly crucial for gold markets, which are experiencing sharp volatility. Gold fell by approximately 1.3% in recent sessions to close near $5,125, yet it remains close to its historical peak reached at the start of the year. If the Fed signals a more hawkish stance, gold may face downward pressure; however, if they express deep concern over geopolitics and inflation, gold could test levels between $5,200 and $5,500.

The Week Ahead: A Decisive Turning Point

Markets await a series of critical meetings:

Federal Reserve: March 17-18, 2026.

ECB & Bank of England: March 19, 2026.

PPI Data: Wednesday, March 18, which will serve as an early indicator of inflation and directly impact the Dollar, Gold, and Bond yields.