Last week saw significant developments across geopolitical tensions in the Middle East, key economic indicators from major economies, and updates on monetary policy. Here’s a comprehensive overview.

Geopolitical Tensions Lead Market Sentiment

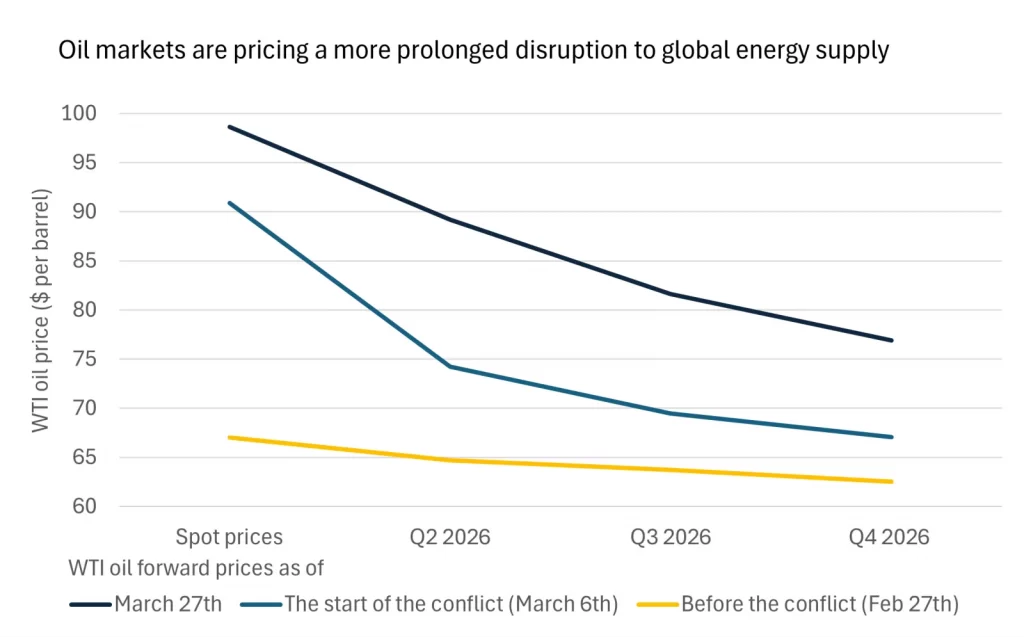

Geopolitical factors dominated market movements last week. The ongoing conflict involving Iran drove global prices of oil and other energy products sharply higher, increasing market volatility and raising fears of a prolonged energy price shock.

This surge has fueled expectations of renewed inflationary pressures. Rising oil and gasoline prices are projected to push headline inflation back up to around 3.5% year-over-year, potentially delaying progress toward the Federal Reserve’s inflation target by another year.

While growth forecasts remain strong, they are increasingly imbalanced. Higher inflation and tighter financial conditions could weigh on consumer spending, housing, and interest-sensitive sectors. Nevertheless, the economy is expected to remain resilient unless the energy crisis worsens.

In this environment, the Federal Reserve faces a difficult task. Markets currently see only a slim chance of another rate hike this year. We believe further monetary tightening is unlikely unless inflation accelerates significantly. The Fed is expected to balance inflation risks against concerns over slowing growth and labor market weakness.

Escalation in Iran

Uncertainty continues to surround the geopolitical situation in the Middle East. Reports suggest a possible expansion of military escalation, including headlines about a potential U.S. ground invasion of Iran.

According to The Washington Post, the U.S. is preparing for “operations inside Iran that could last for weeks,” reflecting a calculated escalation aimed at strengthening its military presence without triggering a full-scale war. The Pentagon is reportedly considering deploying around 3,500 troops for limited raids supported by special forces and other units.

These moves coincide with increased U.S. military presence in the region, including the arrival of the amphibious assault ship USS Tripoli, which leads a naval group of about 3,500 sailors and marines.

The Guardian reported that Washington’s deployment of thousands of troops—including marines and paratroopers—signals clear military readiness. However, this remains contingent on the failure of diplomatic efforts, meaning a ground invasion is not yet imminent.

Iran appears aware of U.S. plans. Iranian media quoted Parliament Speaker Mohammad Bagher Ghalibaf saying, “The U.S. speaks of negotiations publicly but secretly plans a ground attack,” adding that Iranian forces are prepared to punish American allies in the region.

Military experts warn that any U.S. ground operation in Iran would be extremely risky, citing Iran’s vast terrain and the potential for heavy casualties, drawing parallels to Iraq in 2003 and Afghanistan.

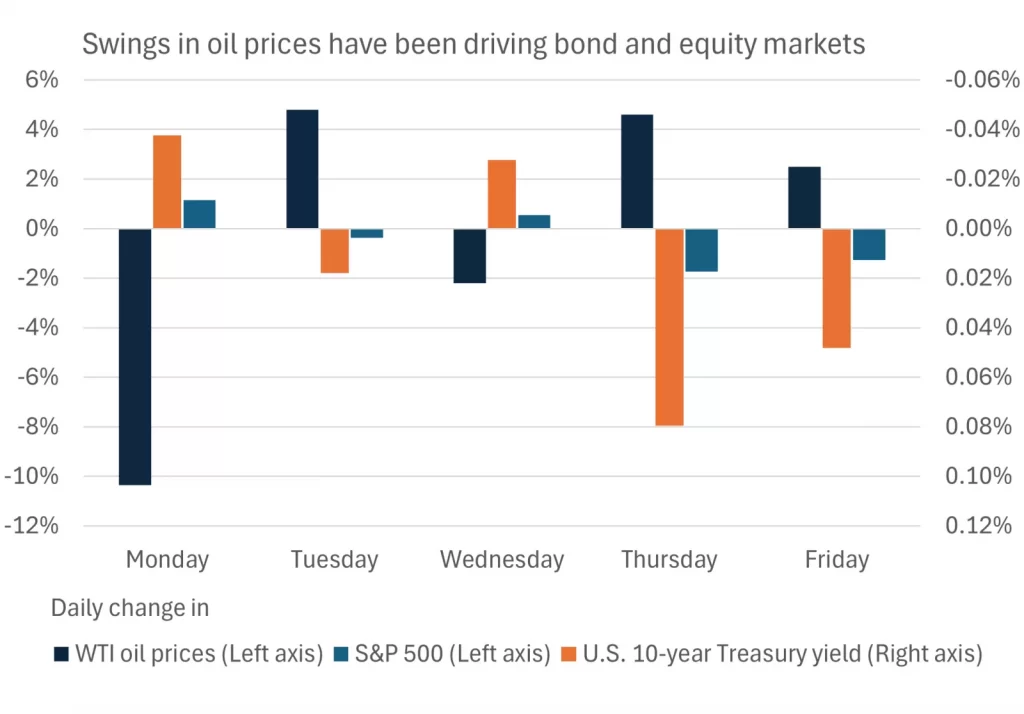

Oil Leads the Gains

Oil prices rose about 3.5% by the end of last week compared to the previous week’s close, driven by continued unrest in the Middle East and the closure of the Strait of Hormuz, through which roughly 20% of global oil supply flows.

This rebound followed a sharp drop earlier in the week due to improved risk appetite after President Trump announced a delay in planned military strikes on Iran’s energy infrastructure. This highlights the uncertainty gripping markets since the conflict began.

Recent developments suggest markets no longer believe in meaningful progress toward de-escalation, especially after Iran denied any talks with the U.S., despite President Trump’s claims of “productive discussions.”

This contradiction has reignited fears of a prolonged conflict, pushing oil prices higher. Continued attacks on energy infrastructure in Iran and Iraq have also raised concerns about producers’ ability to maintain current supply levels.

U.S. Dollar Strengthens

The dollar started last week lower due to improved risk sentiment and weak data. Risk appetite improved after President Trump postponed planned attacks on Iran’s energy infrastructure, a deadline he extended twice.

Negative data also weighed on the dollar, including a drop in the Chicago Fed National Activity Index for February and weaker-than-expected construction spending in January.

However, renewed Israeli attacks on Iran and reports suggesting a U.S. ground invasion may be imminent have reversed the dollar’s trajectory. Most military analysts believe such a move would be highly risky for the U.S., which has supported the dollar’s rebound.

Positive U.S. economic data added further support. Nonfarm productivity held steady at 1.8% in Q4, while unit labor costs were revised up to 4.4%, exceeding expectations. Rising labor costs have heightened inflation concerns, reducing the likelihood of near-term rate cuts.

The dollar also benefited from a stronger-than-expected S&P Global Manufacturing PMI for March, which rose to 52.4, and a sharp improvement in the Richmond Fed Manufacturing Index, which hit a 13-month high.

Weekly jobless claims rose slightly but remained in line with expectations, while continuing claims fell by 32,000 to 1.819 million.

Fed Board Member Steven Miran stated that the central bank still views balance sheet reduction as appropriate despite rising geopolitical and global economic uncertainty—comments that further support the dollar.

With military tensions between the U.S., Israel, and Iran expected to persist, the dollar may continue to gain strength. Fed Chair Jerome Powell’s cautious stance on interest rates amid rising inflation expectations also supports the dollar’s outlook.

Japanese Yen Finds Domestic Support

The yen posted weekly losses due to dollar strength and domestic developments in Japan’s monetary and fiscal policy.

It began the week stronger after Japan’s largest labor union announced wage increases exceeding 5% for the third consecutive year. This supports expectations of further rate hikes by the Bank of Japan, as wage growth is key to sustaining inflation and meeting the bank’s long-term target.

However, improved risk sentiment following Trump’s delay of military action against Iran caused the yen to give up early gains.

Revised data showed Japan’s leading index for January was downgraded to 112.1 from 112.4, signaling slower economic momentum and weakening confidence in the recovery, which added pressure on the yen.

Still, domestic factors favor the yen. Expectations of a rate hike at the next Bank of Japan meeting are rising, supported by wage growth and recent statements from Japan’s Finance Ministry about intervening to prevent excessive currency depreciation.

Euro Awaits Monetary Policy Support

The euro ended last week lower, pressured by dollar strength and deteriorating economic data from the eurozone.

It lost about 0.5% as the dollar continued to benefit from Middle East tensions and strong U.S. data. European consumer confidence also declined, weighing on the euro.

German business sentiment fell sharply, with the IFO Business Climate Index dropping to a 13-month low of 86.4 in March. This reflects ongoing weakness in Europe’s largest economy and raises concerns about eurozone growth prospects.

ECB President Christine Lagarde struck a cautious tone, saying it’s too early to determine the bank’s response to the war’s impact. She noted that the current shock may be less severe than in 2022 due to improved economic conditions, and emphasized the need for more data before taking action—suggesting a wait-and-see approach.

Rising global energy prices have added to the euro’s challenges, as energy is a key driver of eurozone growth.

Bitcoin Continues to Decline

Bitcoin fell at the end of last week, affected by deteriorating risk appetite. It remains closely tied to U.S. equities, especially the S&P 500, making it a risk-sensitive asset.

Cryptocurrencies also suffered from large outflows from spot ETF investment funds. Profit-taking by investors following recent gains added further downward pressure.

Looking Ahead

Markets are now focused on upcoming U.S. employment data, which is expected to be a key driver of global asset prices. March’s jobs report is due Friday, following February’s loss of 92,000 jobs.

Preliminary employment indicators will be released throughout the week, including ADP nonfarm employment change and the Challenger job cuts report.

Concerns over labor market weakness prompted the Fed to cut rates at the end of 2025. Since then, elevated inflation readings have kept rates unchanged. Continued labor market weakness could pressure the Fed to act again.

Other key data this week includes U.S. trade figures and consumer confidence, as well as inflation and consumer sentiment data from Germany and the eurozone, which will help shape the outlook for the euro.

Fed Chair Jerome Powell and FOMC member Austan Goolsbee are also scheduled to speak, and their remarks could significantly impact financial markets.