Global markets endured an extraordinary week of dramatic volatility (ending March 22, 2026). Major central bank decisions collided with escalating geopolitical tensions in the Middle East—specifically the U.S.-Israeli-Iranian conflict. This direct threat to the Strait of Hormuz, a vital artery for 20% of global oil and gas supplies, created a high-voltage economic landscape, leaving its mark on oil, gold, Bitcoin, bonds, and currencies.

Interest Rate Decisions: A United Front Against Inflation

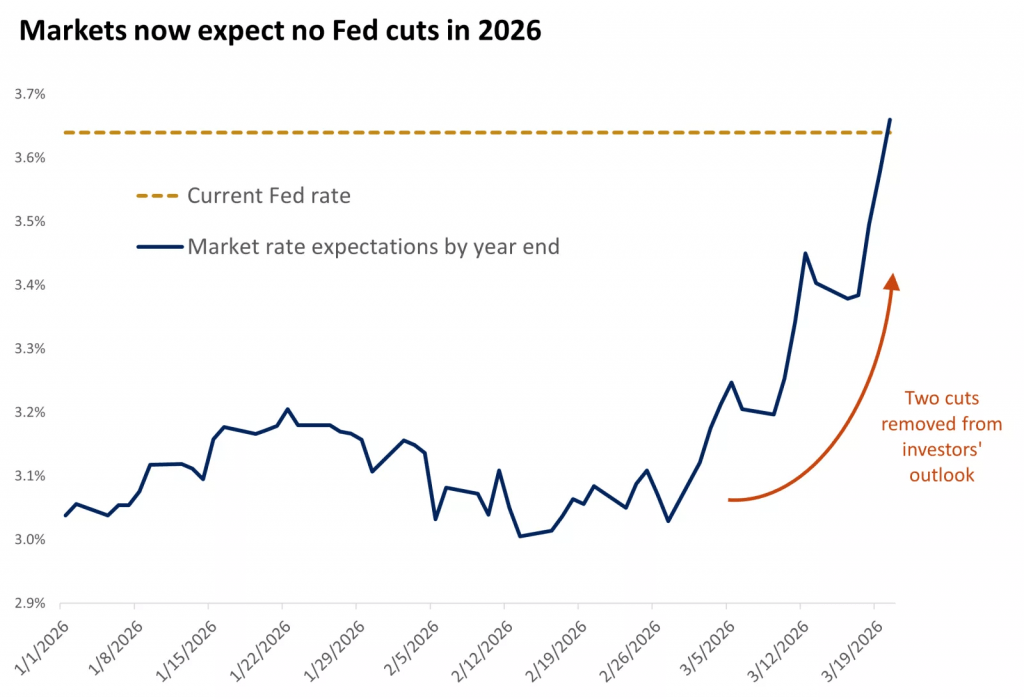

The world’s major central banks delivered a singular, uncompromising message: Inflation remains Public Enemy No. 1.

- The Federal Reserve: Kept rates steady at 3.50%–3.75% (11-1 vote). Chair Jerome Powell signaled that energy-driven inflation precludes any near-term cuts, shattering hopes for a quick pivot.

- The ECB & Bank of England: Both maintained a hawkish stance, with the ECB pricing in potential hikes later this year and the BoE prioritizing inflation control over growth.

- Asia: Central banks in Japan and Indonesia remain on high alert, monitoring the war’s impact on supply chains while leaning toward continued monetary tightening.

Source: Bloomberg

Energy: Supply Shock Pushes Prices Into Triple Digits

Oil prices remained stubbornly above $100 per barrel. Brent crude hovered between $100–$112, while WTI fluctuated between $90–$98. Natural gas saw violent swings amid the U.S.-Iran standoff, prompting the IEA to discuss emergency reserve releases to counter mounting inflationary pressures.

Gold: A Sharp Retreat as the Safe Haven Loses Its Luster

In a surprising twist, gold fell roughly 3% weekly (and up to 10% from previous peaks), sliding to $4,490–$4,494 per ounce. A relatively strong Dollar and surging bond yields have diminished gold’s appeal, even in a high-inflation environment.

Bitcoin & Crypto: Resilience Under Pressure

Bitcoin showed relative stability, holding near $68,500–$69,000. While tight monetary policy dampened risk appetite, continuous institutional inflows into ETFs allowed Bitcoin to outperform gold in terms of price resilience.

Bonds & Currencies: Selling Spree and Dollar Caution

- Bonds: A massive sell-off pushed the 10-year U.S. Treasury yield to 4.28%–4.39%, increasing global borrowing costs.

- Currencies: The USD saw a limited retreat. The EUR/USD stabilized near 1.155, while the Yen rose to 159 per dollar. The Egyptian Pound remained steady at an average of $0.0191.

Strategic Analysis: Is This a 1970s Repeat?

While the “Hormuz shock” is severe, experts argue the global economy is more resilient than it was during the 1970s stagflation for three reasons:

- Consumer Flexibility: Energy now accounts for only 2% of household spending (vs. 6% in the 80s).

- U.S. Energy Independence: The U.S. has been a net exporter since 2019.

- Efficiency: The global economy requires 70% less oil per unit of GDP than it did 50 years ago.

Three Scenarios for the Path Ahead

- Baseline (60%): A sharp but short-lived spike ($90–$100 oil) followed by a modest slowdown and one Fed cut in late 2026.

- Oil Shock (30%): Sustained $120+ oil, pushing inflation to 4%. The Fed stays on hold until 2027, risking a 10-15% market correction.

- De-escalation (10%): A rapid return to $70 oil, allowing two Fed cuts and a massive rally in small-caps and international stocks.

Investment Compass: Where to Position Now?

Despite the “Balance of Terror” at the Fed, solid fundamentals (AI boom and low household debt) provide a cushion.

- If Oil Stays High: Defensive plays in Energy, U.S. Large Caps, and Big Tech are preferred.

- If Tensions Ease: Small Caps, Value Stocks, and International Equities are poised for a breakout.

The Week Ahead

Markets are currently hostages to a volatile mix of geopolitics and hawkish policy. Diversification isn’t just a strategy—it is a survival requirement in this “fog of war” economy. Important economic data for the week ahead includes productivity, S&P Purchasing Managers’ Index (PMI) and consumer sentiment data.