This was by no means an ordinary week. Five consecutive days condensed months of geopolitical tensions into fleeting moments when Iranian Foreign Minister Abbas Araghchi suddenly announced on Friday that the Strait of Hormuz was “fully open” to commercial vessels for the duration of the temporary truce. Those few words were enough to trigger a massive wave across global markets: oil plunged more than 10% in hours, U.S. stocks drifted to new record highs, while gold completed its fourth consecutive winning week, and the Dollar retreated to its lowest levels since the conflict began. Markets, quite simply, bet on peace.

Crude Oil: Extraordinary Volatility in One Week

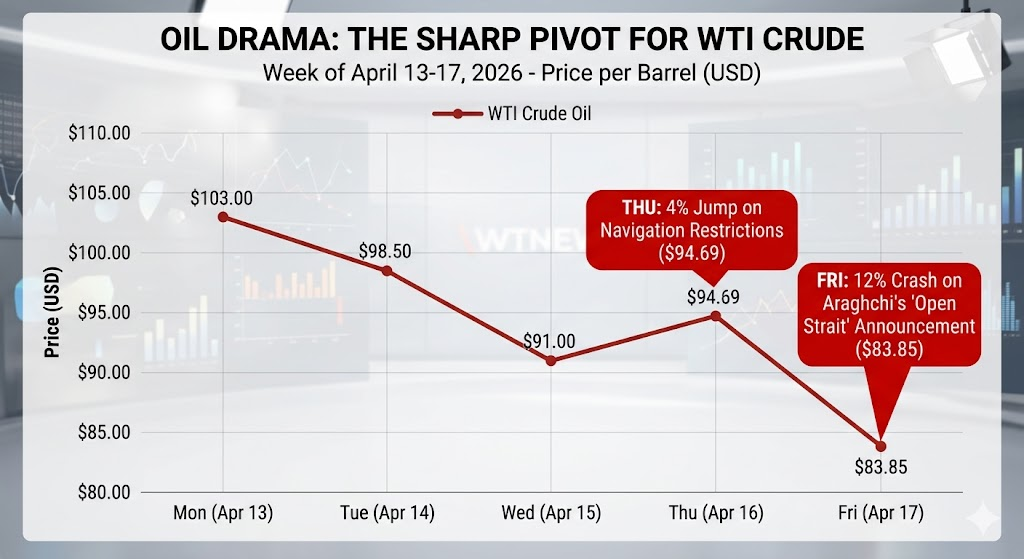

Crude oil was the most dramatic performer this week, shifting from hero to victim in less than 48 hours. Early in the week, Brent maintained levels near $100 per barrel as navigation restrictions continued in the Strait of Hormuz. On Thursday, Brent for June delivery jumped nearly 5% to reach $99.39 per barrel, while West Texas Intermediate (WTI) rose nearly 4% to $94.69, as passage through the strait remained extremely scarce with no clear path to a full reopening.

The truce crashes oil prices, ending a week of extreme volatility – Prepared by Noor Trends Team

However, Friday brought the complete opposite of expectations. WTI futures for May delivery plummeted nearly 12% to close at $83.85 per barrel, while Brent for June delivery lost 9% to close at $90.38. For the week, Brent and WTI declined by approximately 5% and 13% respectively, reversing all accumulated gains from earlier in the week when prices were hitting $103 per barrel.

The broader context puts this drop in perspective: since the start of the U.S.-Iranian conflict on February 28, WTI had peaked at nearly $113 per barrel on April 6, while Brent exceeded $119 on March 30. ING analysts estimate that approximately 13 million barrels per day of supply have been disrupted—a figure that could rise further if the U.S. naval blockade persists.

Gold and Silver: Safe Haven Completes its Run

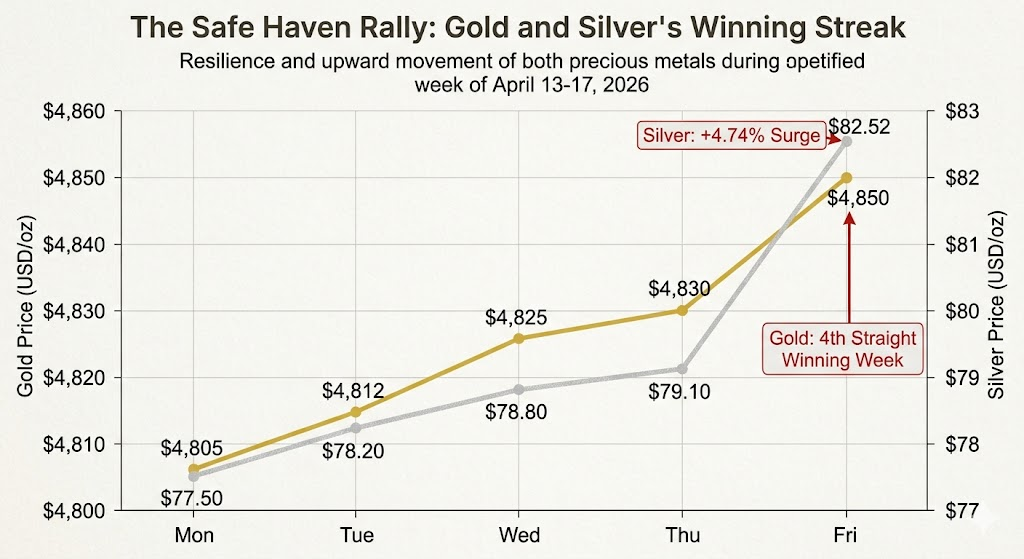

Gold ended the week up 0.8%, completing its fourth consecutive winning streak. The price of gold rose nearly 1% above $4,850 per ounce at Friday’s close, fueled by investor optimism that a permanent agreement between Washington and Tehran could lower inflation risks and reduce the need for monetary tightening by central banks. Gold had surpassed $4,800 per ounce on April 14, representing a year-on-year increase of more than 50%.

Safe havens continue to shine as Silver steals the spotlight – Prepared by Noor Trends Team

Silver was the week’s most exciting star. Silver prices hit $82.52 per ounce in Friday’s session, up 4.74% in a single day—the strongest daily gain of the week. This sharp move narrowed the Gold-Silver ratio to 59.0, reflecting surging industrial and investment demand for the white metal. The structural factor behind gold’s strength remains active behind the scenes: JPMorgan and Goldman Sachs forecast gold to fluctuate within the $4,000–$6,300 range during 2026, given ongoing central bank purchases and continuous geopolitical ambiguity.

Aluminum: A Structural Crisis at the Heart of Global Industry

Of all assets, aluminum was perhaps most exposed to real geopolitical entanglement this week. Aluminum contracts peaked early in the week near $3,670 per ton in the UK—the highest level in four years—before retreating to $3,557 per ton by week’s end, a 2.4% drop in a single day. The immediate cause was the Iranian announcement regarding the strait, which sparked hopes for the return of Gulf exports. However, the structural picture remains concerning: Emirates Global Aluminium, the region’s largest producer, declared force majeure on some deliveries following a smelter shutdown in Al Taweelah. Bahrain’s Alba was also affected, while Qatar Aluminium had previously cut production due to energy crises. Wood Mackenzie estimates a global deficit of 4 million metric tons during 2026. Compared to last year, aluminum prices are up 48.55% annually.

U.S. Equities: Earnings Season Ignites a Market Ready for Recovery

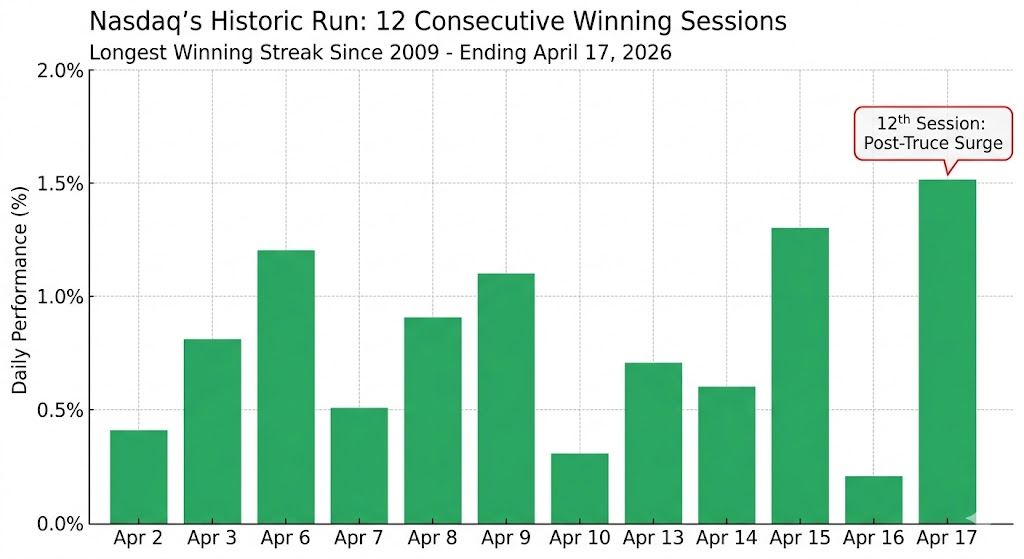

Wall Street witnessed one of its strongest weeks of 2026. The S&P 500 closed Thursday at 7,041.28 points, up 0.26%, while the Nasdaq completed its 12th consecutive winning streak—the longest since 2009. On Friday, the Dow Jones jumped 869 points (1.79%) to close at 49,447, while the S&P 500 rose 1.2% and the Nasdaq 100 gained 1.5% following the Iranian announcement. For the week, the S&P 500 and Nasdaq rose 3.3% and 5.2% respectively, while the Dow added more than 1%.

Nasdaq hits its longest winning streak since 2009 – Prepared by Noor Trends Team

Earnings Highlights: A Season Starting Mid-Crisis

The Q1 2026 earnings season kicked off last week under exceptional circumstances imposed by war and rising costs. However, the figures largely exceeded street expectations, adding further fuel to the market rally.

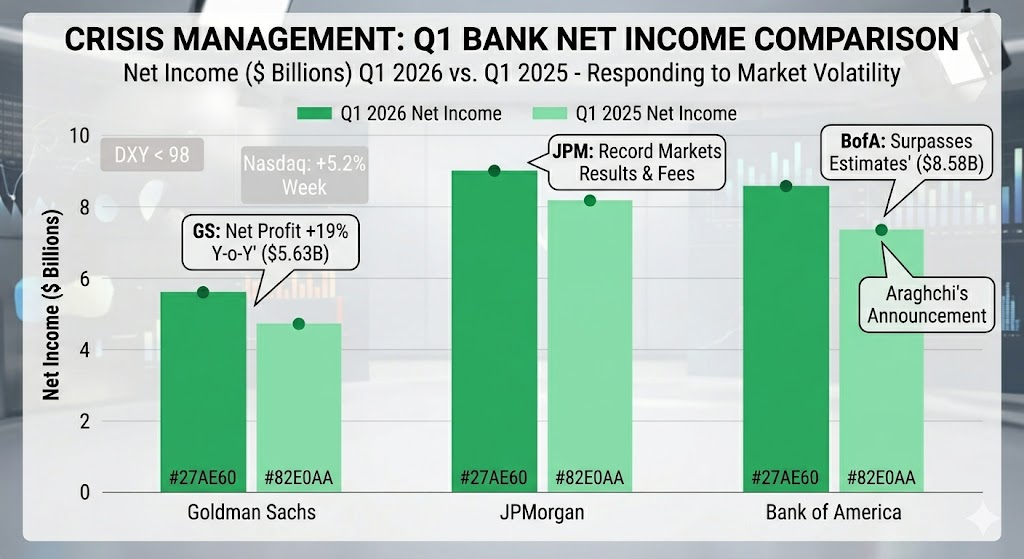

Goldman Sachs: Sparked the rally on Monday with impressive results, reporting net revenues of $17.23 billion and net earnings of $5.63 billion for the quarter ending March 2026, up 19% in profit and 14% in revenue year-on-year.

JPMorgan: Beat expectations thanks to record results in the markets division and a sharp rise in underwriting fees, with revenues growing 10% annually.

Record profits for major banks despite geopolitical challenges – Prepared by Noor Trends Team

Bank of America: Recorded a net profit of $8.58 billion in Q1 2026, up from $7.36 billion in Q1 2025, with total revenues of $30.27 billion, surpassing analyst estimates.

Netflix: Beat Wall Street expectations on both earnings and revenue, yet its stock plunged as much as 10% in after-hours trading due to the announced departure of co-founder Reed Hastings from the board.

ASML & PepsiCo: ASML raised its annual revenue guidance to the €36–40 billion range, citing AI infrastructure demand. PepsiCo surprised with strong results, with revenues rising 8.5% to $19.44 billion.

European and Asian Markets: Uneven Recovery

The German DAX ended the week at 24,702.24 points, rising 2.27% in Friday’s session alone. France’s CAC 40 closed at 8,425.13 points with a 1.97% gain. For the week, the DAX added 3.77%, Italy’s FTSE MIB rose 2.65%, while the UK’s FTSE 100 settled for a modest 0.63% gain. The IMF warned of a potential major energy crisis hitting the Eurozone if the conflict is not resolved quickly, lowering the bloc’s 2026 growth forecast to 1.1%.

In Asia, Japan’s Nikkei 225 added 2.73% for the week to hit a historic peak, while major Chinese exchanges remained nearly flat. The Shanghai Composite fell slightly by 0.10%, and the Hang Seng dropped 0.89%. China’s GDP grew 5% annually in Q1 2026, but retail sales slowed to 1.7% and real estate investment continued to contract by 11.2%.

Cryptocurrencies: Reconciling with Optimism

Bitcoin rose 5% within 24 hours early in the week to reach approximately $75,000. Meanwhile, Ethereum jumped 7% in a single day to nearly $2,400. Friday was the hottest day, as Bitcoin surged to about $77,400 following the announcement of the strait opening, while Ethereum climbed to $2,440 and Solana jumped above $90. While prices remain below the October 2025 peak of $126,198, they have risen about 25% from the 2026 bottom near $60,000, supported by steady inflows into Bitcoin ETFs and growing institutional adoption.

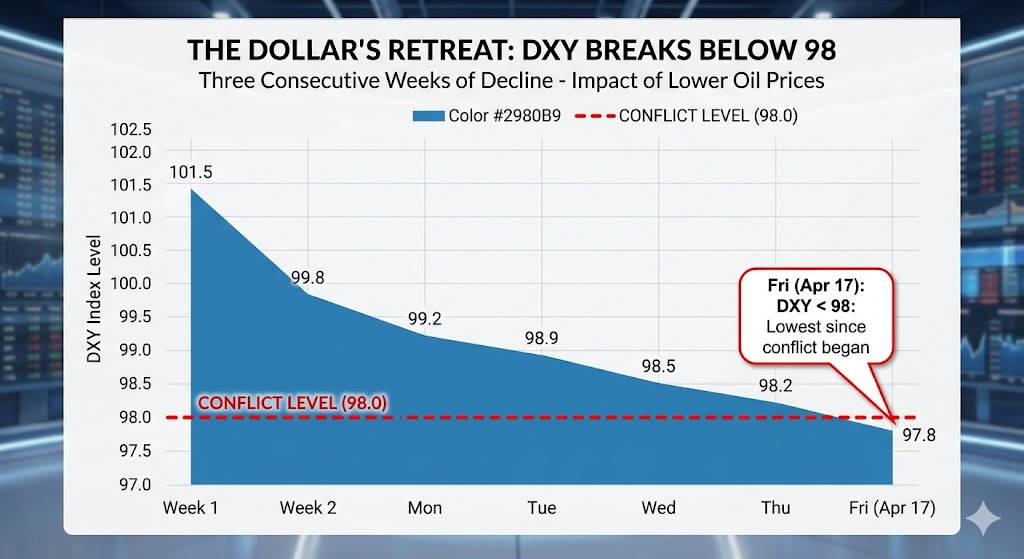

Dollar and Traditional Currencies: Third Consecutive Weekly Decline

The Dollar Index (DXY) fell below 98 points on Friday, marking its lowest levels since the outbreak of the Iranian conflict. Lower oil prices helped ease inflation expectations and reduced bets on aggressive Fed tightening. For the week, the DXY fell approximately 0.5% for its third consecutive losing week. Derivatives markets are now pricing in a 50-50 chance of a 25-basis-point rate cut by year-end.

DXY Performance – Prepared by Noor Trends Team

Central Banks and Policy Outlook: Four Divergent Paths

U.S. Federal Reserve: NY Fed President John Williams emphasized that high uncertainty should limit forward guidance. The major event is the Senate hearing on Tuesday, April 21, for nominee Kevin Warsh to succeed Jerome Powell, whose term ends May 15.

European Central Bank: Held the deposit rate at 2.0% in its March 19 meeting, noting that Middle East conflict would push short-term inflation higher. The priority remains data monitoring before any move.

Bank of England: Reported UK inflation at 3.0% in January, above the 2% target. The bank expects inflation to rise to 3–3.5% in coming quarters due to high energy prices, pledging to monitor developments closely ahead of the April 30 meeting.

Bank of Japan: Expectations for an April rate hike faded, reflecting caution amid global energy disruptions. The Yen continued to strengthen as a safe haven.

Economic Data: Looking Back and Ahead

Data Released (April 13–17):

Weekly jobless claims fell to 207,000, indicating a resilient labor market. Core CPI for March was better than expected, growing 0.2% monthly, signaling an initial easing of some soft inflationary pressures.

Upcoming Economic Dates (April 20–24):

Next week is one of the busiest of 2026. The agenda is dominated by the Senate hearing for Fed nominee Kevin Warsh on Tuesday, April 21, at 10:00 AM ET. On the data front, Wednesday brings ADP private employment changes, followed by jobless claims and PMI data for manufacturing and services on Thursday. Friday features the University of Michigan Consumer Sentiment index. In earnings, Tesla reports Wednesday after the close, alongside defense giants like Northrop Grumman and Lockheed Martin. Investors will also closely watch the expiration of the U.S.-Iranian truce on Tuesday, April 21.

Friday Was a Game-Changer

The week of April 13–17, 2026, was not just about numbers on trading screens; it was a real-world test of how global markets absorb sudden geopolitical shifts. Gold, Silver, and Bitcoin maintained their safe-haven status, while oil—up 50% since the war began—faced its biggest one-day drop in months. The VIX volatility index closed at 17.48, down 2.56%, suggesting the market is starting to digest some geopolitical improvement, though it is not yet pricing in total peace. The coming phase will determine if this is the start of a true pivot or just a temporary pause on a long road.